Andhra Pradesh BIEAP AP Inter 2nd Year Accountancy Study Material 6th Lesson Admission of a Partner Textbook Questions and Answers.

AP Inter 2nd Year Accountancy Study Material 6th Lesson Admission of a Partner

Very Short Answer Questions

Question 1.

What are the aspects that need adjustment at the time of admission of a new partner?

Answer:

When a new partner is admitted to the firm the agreement among the existing partners terminates and a new agreement will come into force.

The following adjustments must be made at the time of admission.

- New profit sharing ratio.

- Revaluation of assets and liabilities.

- Distribution of accumulated reserves, profits/losses.

- Treatment of goodwill.

- Adjustment of partners’ capitals.

Question 2.

Sacrificing Ratio

Answer:

The ratio in which the old partners agree to sacrifice their share of profit in favour of the incoming partner is called sacrificing ratio.

Sacrificing Ratio = Old share of Profit – New share of Profit.

Question 3.

Revaluation Account

Answer:

For the purpose of revaluation of assets and liabilities at the time of admission of a new partner, an account called a revaluation account is opened. It is a nominal account. The account is credited with all increases in the value of assets and decreases in the value of liabilities. Similarly, it is debited with a decrease in the value of assets and an increase in the value of liabilities. The balance of this account is again or lost on revaluation which is transferred to the old partners’ capital accounts in the old profit sharing ratio.

![]()

Question 4.

Goodwill

Answer:

Over a period of time, a well-established business develops the advantage of a good name and reputation which helps the business to earn more profits. The monetary value is called goodwill. It is regarded as an intangible asset. So, goodwill is the value of the reputation of a firm in respect of profits expected in the future over and above normal profits.

Question 5.

What are the methods of goodwill valuation?

Answer:

The important methods of valuation of Goodwill are:

1. Average profits method: Under this method, the goodwill is valued at an agreed number of years of the purchase of the average profits of the past few years.

Goodwill = Average profit × No. of years purchase

2. Super profit method: Super profit is the profit earned by the business in excess of the usual profit goodwill is valued by multiplying the super profit by the number of years purchased.

3. Capitalisation method: Under capitalisation method, the capitalized value of the business is determined by capitalizing the average profits by the normal rate of return. Out of the value so determined, the value of net assets/ capital employed is deducted, and the balance amount is the value of goodwill.

Textual Problems

Question 1.

M and N are partners sharing profit and losses in the 1 : 2 ratio. They have decided to admit ‘O’ by giving him 1/4th share in future profits. Calculate the New profit sharing ratio.

Solution:

If we assume the total share is 1

The new partners share is a \(\frac{1}{4}\)

Remaining share = 1 – \(\frac{1}{4}\) = \(\frac{3}{4}\)

Old Ratio = 1 : 2

New Share = Rest of the share × old ratio

M new share = \(\frac{3}{4} \times \frac{1}{3}=\frac{3}{12}\)

N new share = \(\frac{3}{4} \times \frac{2}{3}=\frac{6}{12}\)

O’s Share = \(\frac{1}{4}\) or \(\frac{3}{12}\)

New Share = 1 : 2 : 1

Question 2.

P & Q are partners sharing in the ratio of 2 : 3. They admit R for 1/4th share and he gets this share equally from P & Q. Calculate the new ratio.

Solution:

New partner R share \(\frac{1}{4}\)

He gets this equally from P and Q. That is \(\frac{1}{4} \times \frac{1}{2}=\frac{1}{8}\)

Old Ratio = 2 : 3

New Share = Old share – Sacrificing ratio

P = \(\frac{2}{5}-\frac{1}{8}=\frac{16}{40}-\frac{5}{40}=\frac{11}{40}\)

Q = \(\frac{3}{5}-\frac{1}{8}=\frac{24}{40}-\frac{5}{40}=\frac{19}{40}\)

R = \(\frac{1}{4}\) or \(\frac{10}{40}\)

Question 3.

X and Y share profits and losses in the Ratio of 4 : 3, they admit Z with 3/7th share; which he gets 2/7th from X and 1/7th from Y. What is the new profit sharing ratio?

Solution:

New partner Z’s share = \(\frac{3}{7}\) (This acquired \(\frac{2}{7}\) from X and \(\frac{1}{7}\) from Y)

Old ratio = 4 : 3

New share = Old share – Sacrificing ratio

X = \(\frac{4}{7}-\frac{2}{7}=\frac{2}{7}\)

Y = \(\frac{3}{7}-\frac{1}{7}=\frac{2}{7}\)

Z = \(\frac{3}{7}\)

![]()

Question 4.

A & B are partners sharing in the ratio of 3 : 2. C is admitted and he gets 3/20th from A and 1/20th from B. Calculate the new ratio.

Solution:

C’s share = \(\frac{4}{20}\) (Acquires \(\frac{3}{20}\) from A, \(\frac{1}{20}\) from B)

Old ratio = 3 : 2

New share = Old share – Sacrificing ratio

A = \(\frac{3}{5}-\frac{3}{20} \text { or } \frac{12}{20}-\frac{3}{20}=\frac{9}{20}\)

B = \(\frac{2}{5}-\frac{1}{20} \text { or } \frac{8}{20}-\frac{1}{20}=\frac{7}{20}\)

C = \(\frac{4}{20}\)

New ratio = 9 : 7 : 4

Question 5.

X & Y are partners who share profits in the ratio of 5 : 3. Z the new partner gets 1/5 of X’s share and 1/3rd of Y’s share. Calculate the new ratio.

Solution:

Z gets \(\frac{1}{5}\) share from X and \(\frac{1}{3}\) share from Y

Old ratio = 5 : 3

New ratio = Old ratio – Sacrificing ratio

X share = \(\frac{5}{8}-\frac{1}{5} \text { or } \frac{25}{40}-\frac{8}{40}=\frac{17}{40}\)

Y share = \(\frac{3}{8}-\frac{1}{3}=\frac{9}{24}-\frac{8}{24}=\frac{1}{24}\)

Z share = \(\frac{1}{5}+\frac{1}{3} \text { or } \frac{3}{15}+\frac{5}{15}=\frac{8}{15}\)

Question 6.

If Tarun and Nisha are partners sharing profits in the ratio of 5 : 3. What will be their sacrificing ratio if Rahul is admitted for 1/8 share of profit in the firm?

Solution:

Rahul share = \(\frac{1}{8}\)

Remaining share = 1 – \(\frac{1}{8}\) = \(\frac{7}{8}\)

New ratio:

Tarun = \(\frac{7}{8} \times \frac{5}{8}=\frac{35}{64}\)

Nisha = \(\frac{7}{8} \times \frac{3}{8}=\frac{21}{64}\)

Rahul \(\frac{1}{8}\) or \(\frac{8}{64}\)

Sacrificing ratio = Old ratio – New ratio

Tarun = \(\frac{5}{8}-\frac{35}{64} \text { or } \frac{40}{64}-\frac{35}{64}=\frac{5}{64}\)

Nisha = \(\frac{3}{8}-\frac{21}{64}=\frac{24}{64}-\frac{21}{24}=\frac{3}{24}\)

So Sacrificing ratio = 5 : 3

Question 7.

Amar and Bahadur are partners in firm sharing profits in the ratio of 5 : 2. They admitted Mary as a new partner for 1/4 share. The new profit sharing ratio of the partners will be 2 : 1 : 1. Calculate their sacrificing ratio.

Solution:

Old ratio = 5 : 2

New ratio = 2 : 1 : 1

Amar old ratio = \(\frac{5}{7}\)

Amar new ratio = \(\frac{2}{4}\)

Sacrificing ratio = old ratio – new ratio

Amar = \(\frac{5}{7}-\frac{2}{4}=\frac{20-14}{18}=\frac{6}{28}\)

Bahadur = \(\frac{2}{7}-\frac{1}{4}=\frac{8-7}{28}=\frac{1}{28}\)

∴ So sacrificing ratio = 6 : 1

![]()

Question 8.

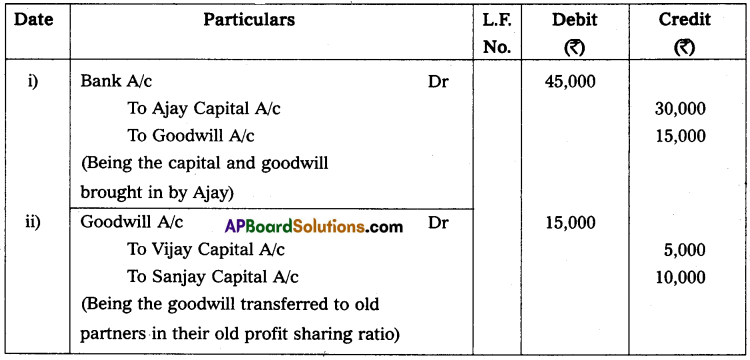

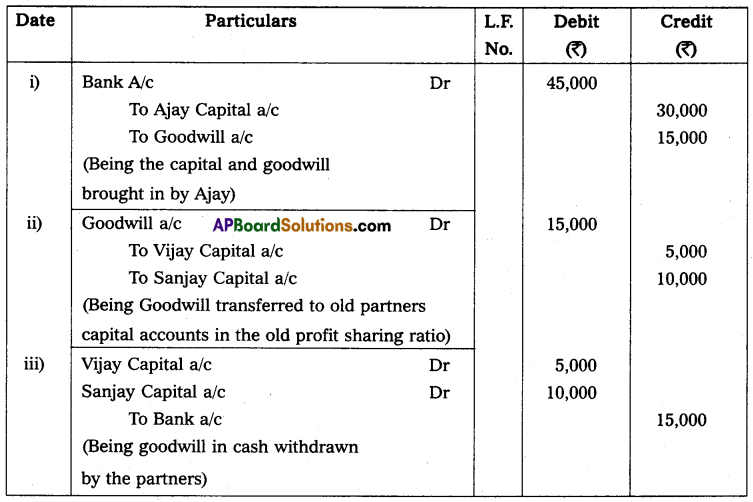

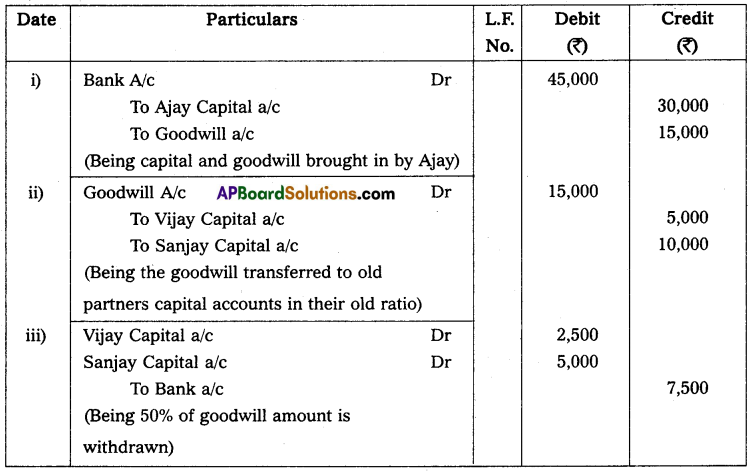

Vijay and Sanjay are partners in the firm sharing profits and losses in the ratio of 1 : 2. They decide to admit Ajay into partnership with 1/4 share in profits. Ajay brings in ₹ 30,000 for capital and ₹ 15,000 for goodwill. Give necessary journal entries,

(a) When the amount of goodwill is retained in the business.

(b) When the amount of goodwill is fully withdrawn.

(c) When 50% of the amount of goodwill is withdrawn.

Solution:

(a) When the amount of goodwill is retained in the business.

(b) When the amount of goodwill is fully withdrawn

(c) When 50% of the amount of goodwill is withdrawn

Question 9.

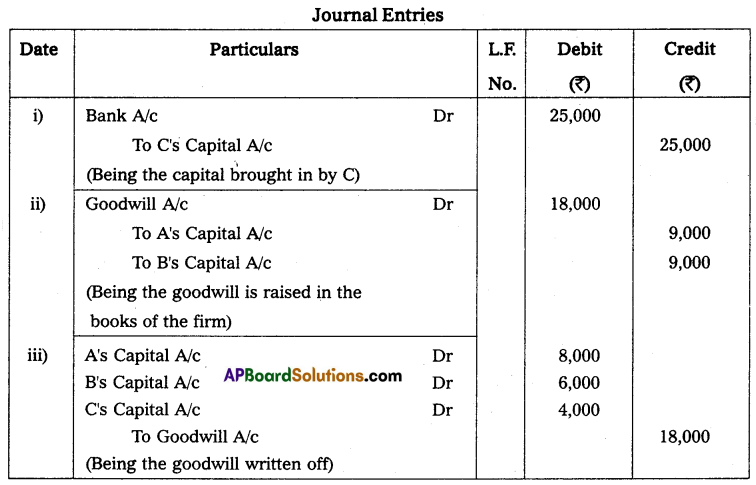

A and B are partners sharing profits and losses equally. They admit C into partnership and the new ratio is fixed as 4 : 3 : 2. C is unable to bring anything for goodwill but brings ₹ 25,000 as capital. Goodwill of the firm is valued at ₹ 18,000. Give the necessary journal entries assuming that the partners do not want goodwill to appear on the Balance Sheet.

Solution:

Question 10.

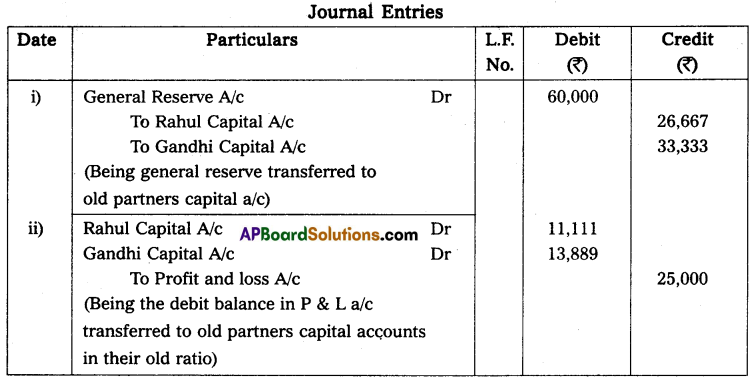

Rahul and Gandhi are partners sharing profit in the ratio of 4 : 5. On 1st April 2015, they admit Sonia as a new partner for 1/6 share in profits. On that date, the balance sheet of the firm shows a balance of ₹ 60,000 in general reserve and a debit balance of Profit and Loss A/c of ₹ 25,000.

Make the necessary journal entries.

Solution:

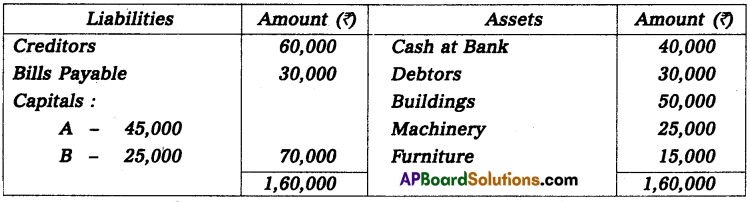

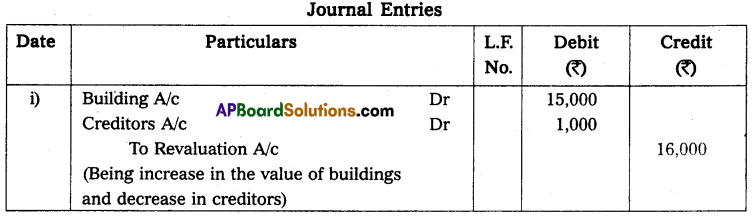

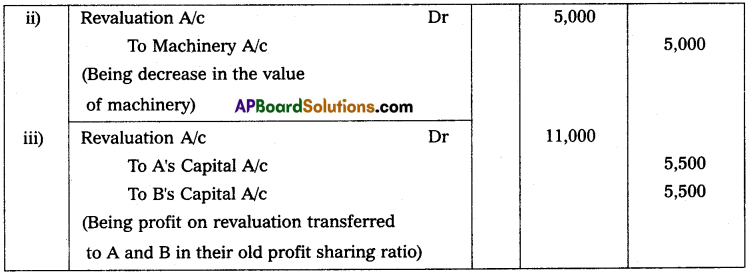

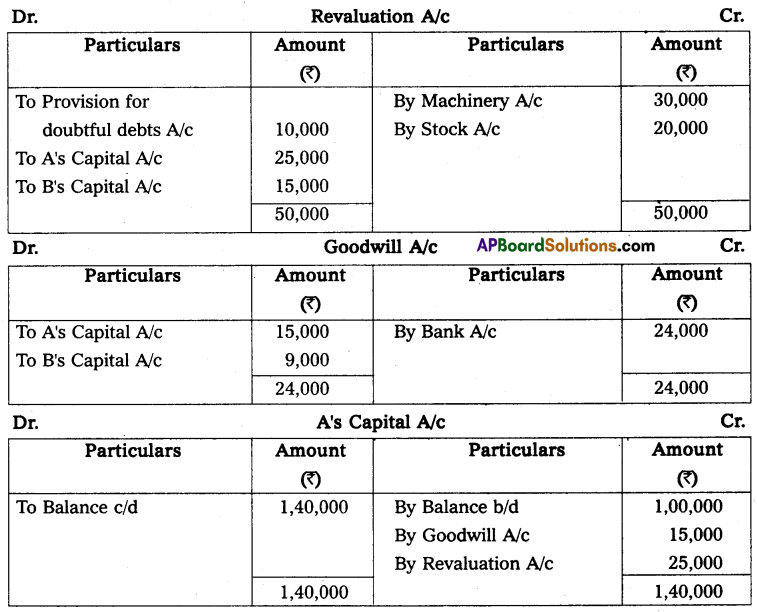

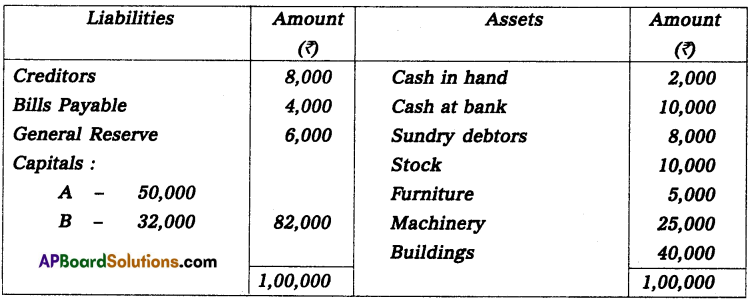

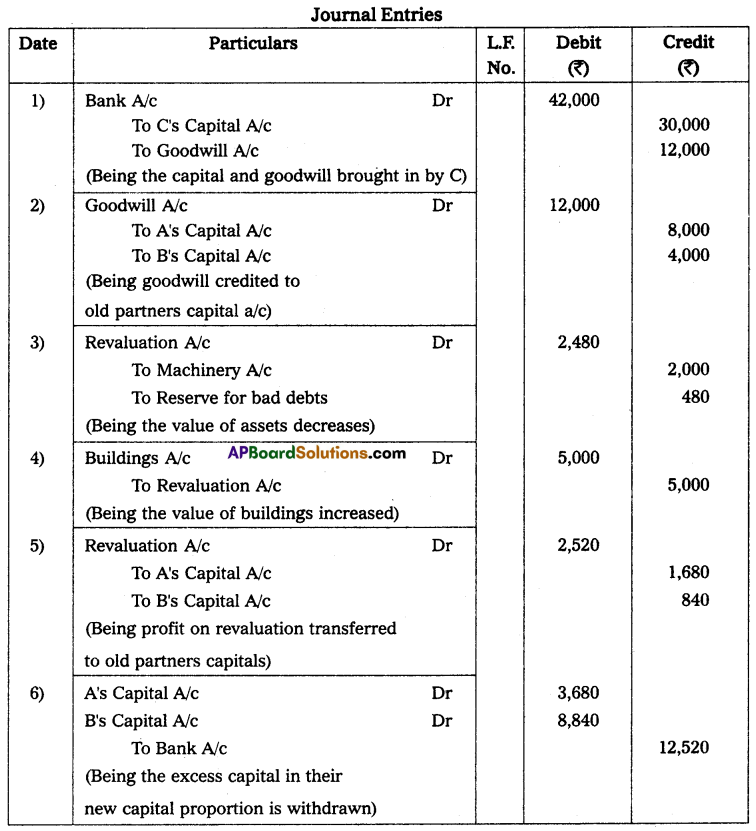

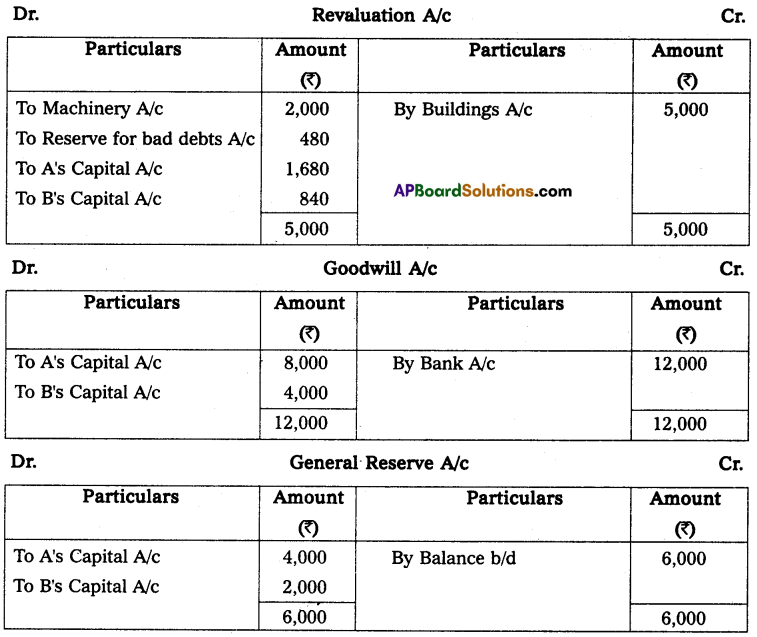

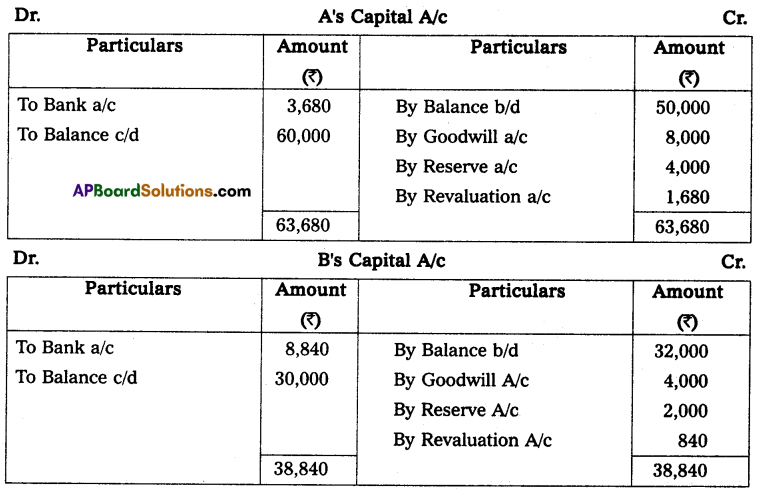

Question 11.

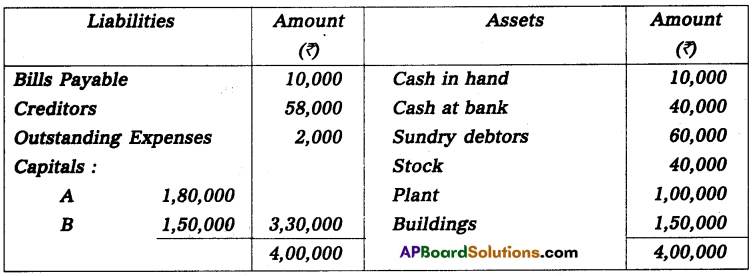

A & B are equal partners in a firm. They decide to admit C as a new partner for 1/5th share in profit. On the date of admission the balance sheet of the firm was as follows:

The terms of the agreement on C’s admission were as follows:

(a) Building will be valued at ₹ 65,000 and machinery at ₹ 20,000

(b) Creditors included ₹ 1,000 no longer payable.

Pass necessary Journal entries for revaluation of assets and liabilities.

Solution:

![]()

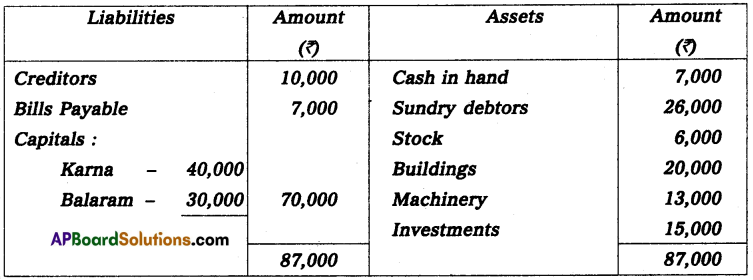

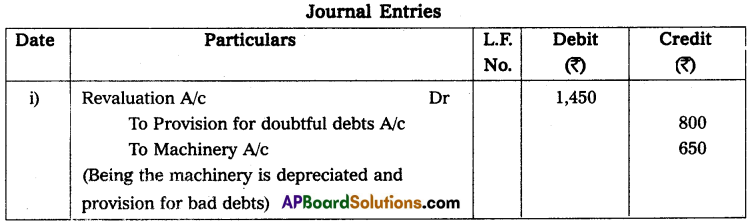

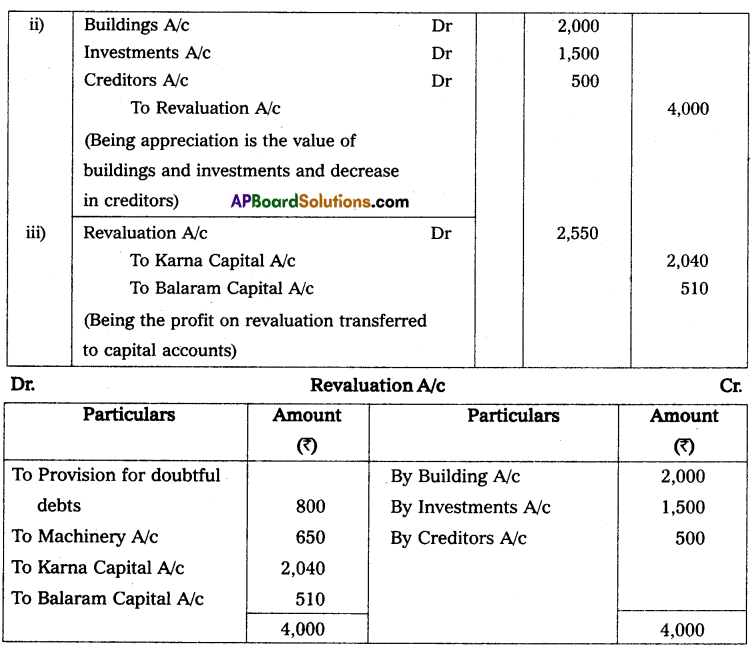

Question 12.

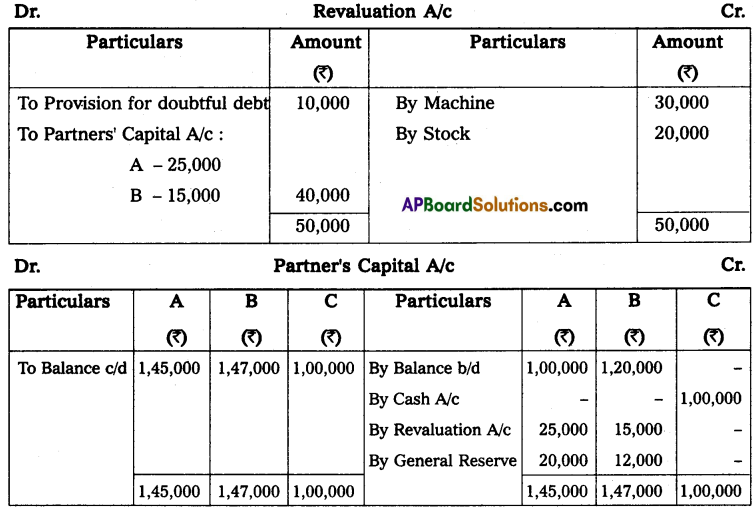

Kama and Balaram are partners sharing profit and losses in the ratio of 4 : 1. Their Balance Sheet was as follows:

Balance Sheet of Kama and Balaram as of December 31st, 2014

Nikhil is admitted as a partner and assets are revalued and liabilities reassessed as follows:

(i) Create a Provision for doubtful debt on debtors at ₹ 800

(ii) Building and investment are appreciated by 10%.

(iii) Machinery is deprecated at 5%

(iv) Creditors were overestimated by ₹ 500

Make journal entries and Prepare a revaluation account before the admission of Nikhil.

Solution:

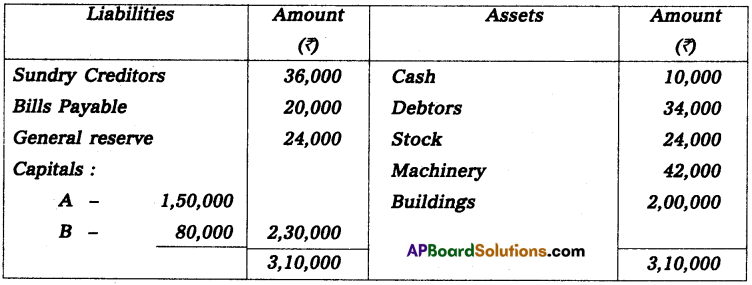

Question 13.

Balance Sheet of A and B as on 31.03.2014

The other terms of the agreement on C’s admission were as follows:

(i) C will bring ₹ 12,000 for his share of capital.

(ii) Building will be valued at ₹ 1,85,000 and Machinery at ₹ 40,000

(iii) A provision of 6% will be created for debtors with bad debts.

Prepare Revaluation Account and Partners Capital Accounts.

Solution:

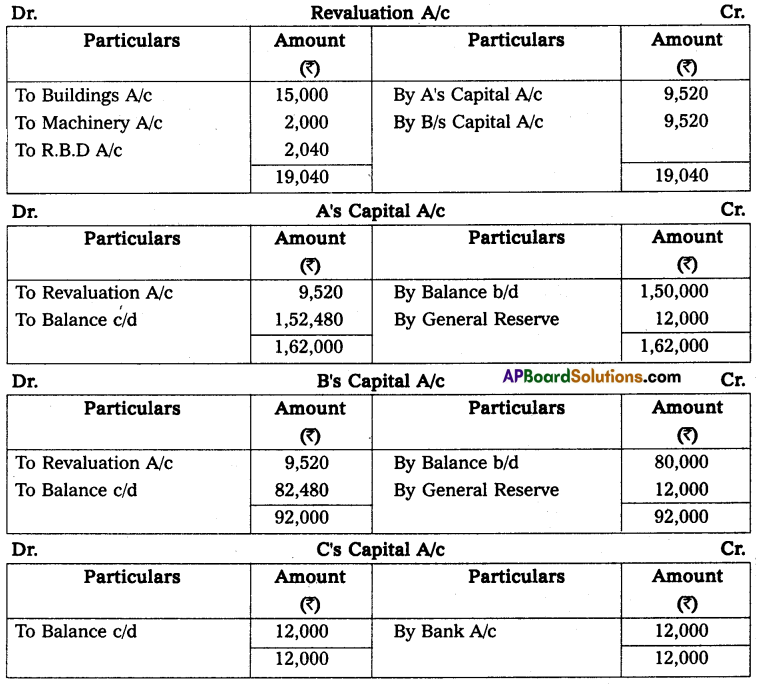

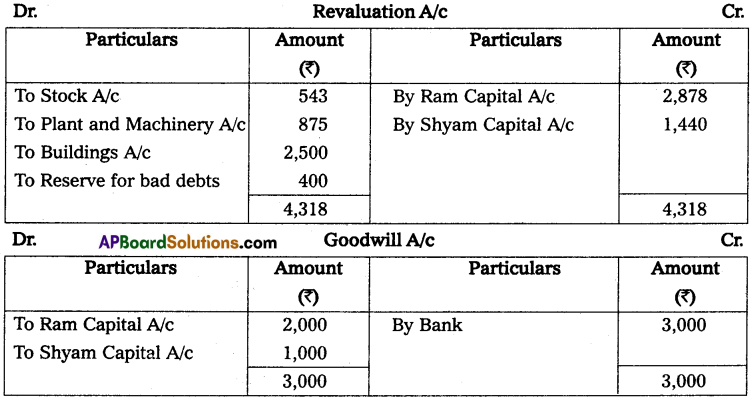

Question 14.

The following is the balance sheet of Ram and Shyam, who are sharing profit as 2/3 and 1/3 on 31st March 2014.

They agree to admit Mohan into partnership on the following terms:

(a) Mohan was to be given 1/3 share in the profit and to bring ₹ 7,500 as his capital and ₹ 3,000 as his share of goodwill.

(b) That the value of stock and plant & Machinery was to be reduced by 5%.

(c) That a reserve of 10% was to be created in respect of Sundry Debtors.

(d) The buildings were to be depreciated by 10%.

Pass Journal Entries and necessary Accounts.

Solution:

![]()

Question 15.

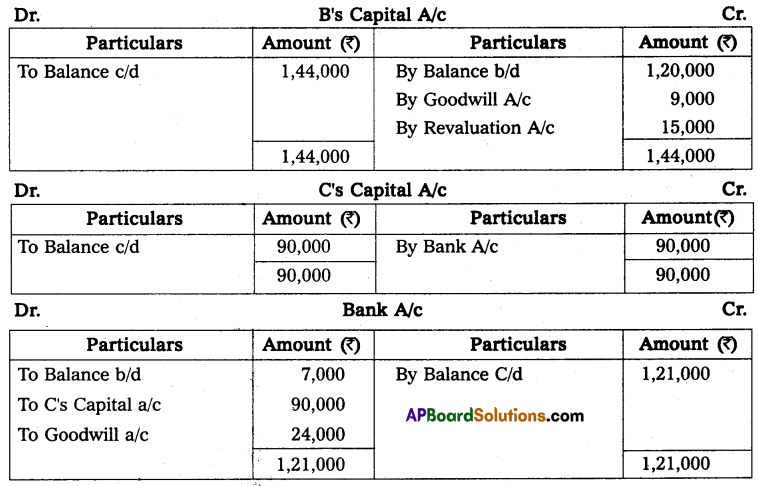

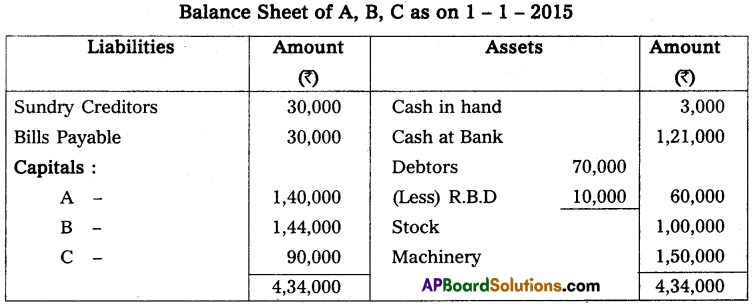

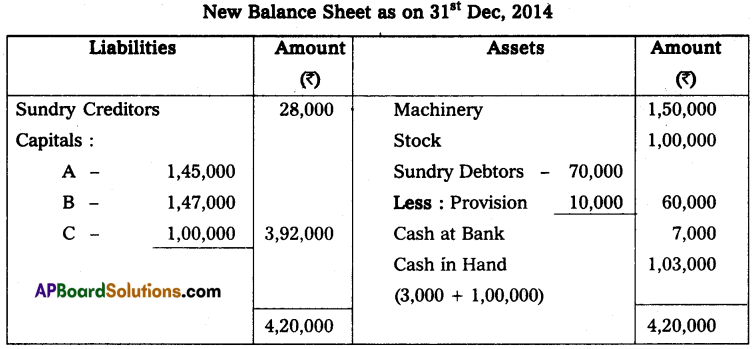

A and B are partners in a firm, sharing profits and losses in the ratio of 5 : 3, on 31st December 2014 their Balance sheet was as under:

On the above date they decided to admit C as a partner on the following terms:

(a) C will bring ₹ 90,000 as his capital and ₹ 24,000 for his share of goodwill for 1/4th share in the profit.

(b) Machinery is to be valued at ₹ 1,50,000, stock ₹ 1,00,000, and provision for bad debts of ₹ 10,000 is to be created.

Prepare Revaluation A/c, partners’ capital A/c and new Balance Sheet.

Solution:

Question 16.

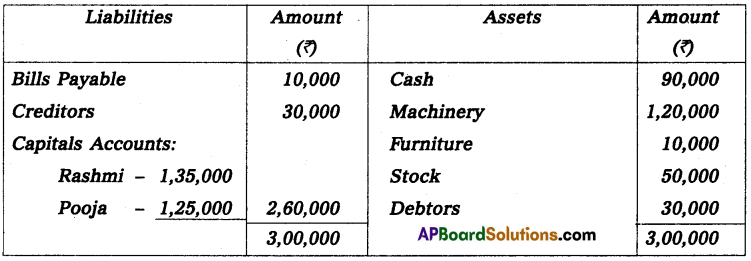

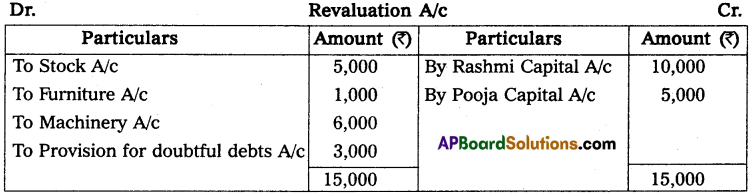

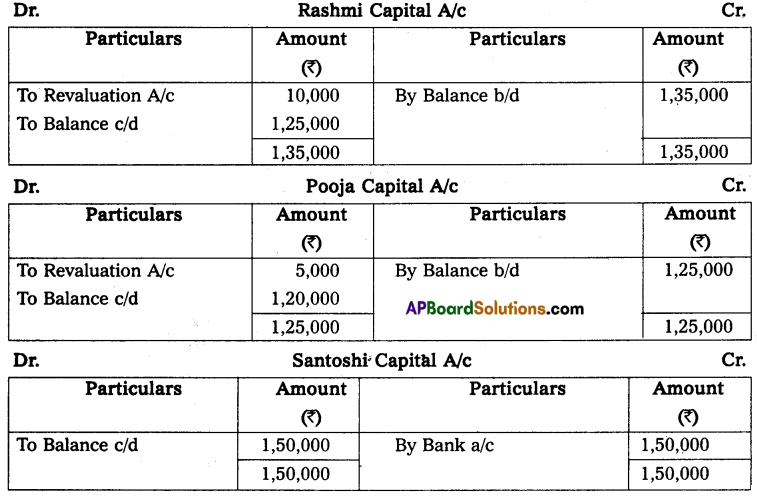

Rashmi and Pooja are partners in a firm. They share profits and losses in the ratio of 2 : 1. They admit Santoshi into a partnership firm on the condition that she will bring ₹ 1,50,000 for capital and she will be given 1/3 share in future profits. At the time of admission on the Balance Sheet of Rashmi and Pooja was as under.

It was decided to:

(a) Revaluate stock at ₹ 45,000.

(b) Depreciate furniture by 10% and machinery by 5%.

(c) Make provision of ₹ 3,000 on sundry debtors for doubtful debts.

Prepare Revaluation Accounts, Partners Capital Accounts, and Balance Sheet of the new firm.

Solution:

![]()

Question 17.

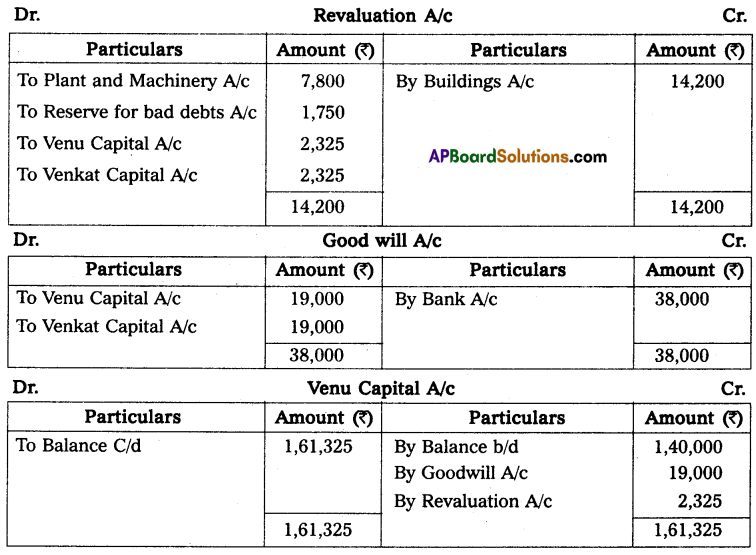

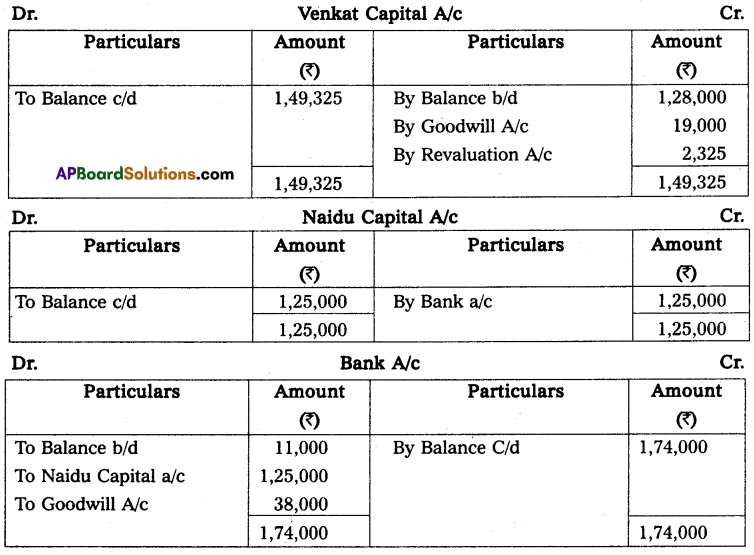

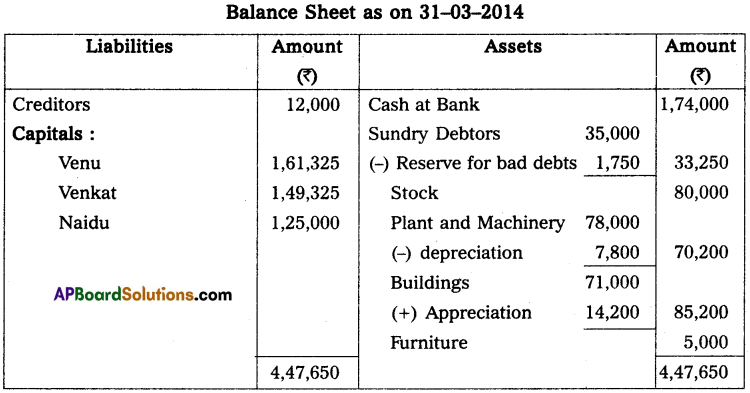

Venu & Venkat are partners in a business sharing profits and losses equally. Their Balance Sheet on 31-3-2014 stood as under;

They decided to admit Naidu into the firm on 1st April 2014 on the following terms and conditions:

(a) Naidu has to pay ₹ 1,25,000/- for 1/4 share in future profits.

(b) Naidu has to pay ₹ 38,000/- for goodwill.

(c) Plant and Machinery to be depreciated by 10%.

(d) Buildings to be appreciated by 20%.

(e) 5% reserve for doubt full debts to be created on debtors.

Prepare necessary accounts in the books of the firm after admission of Naidu with the new Balance Sheet.

Solution:

Question 18.

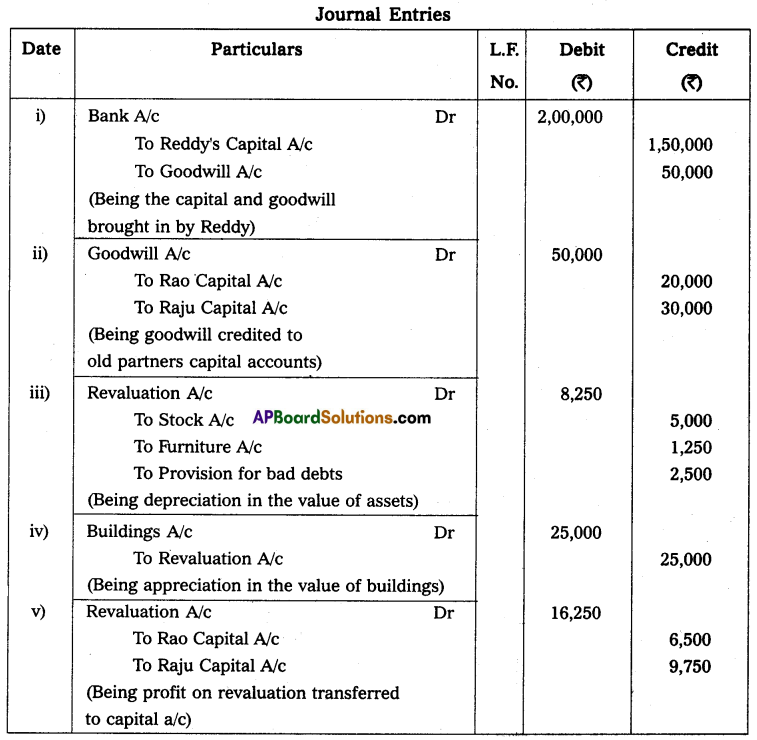

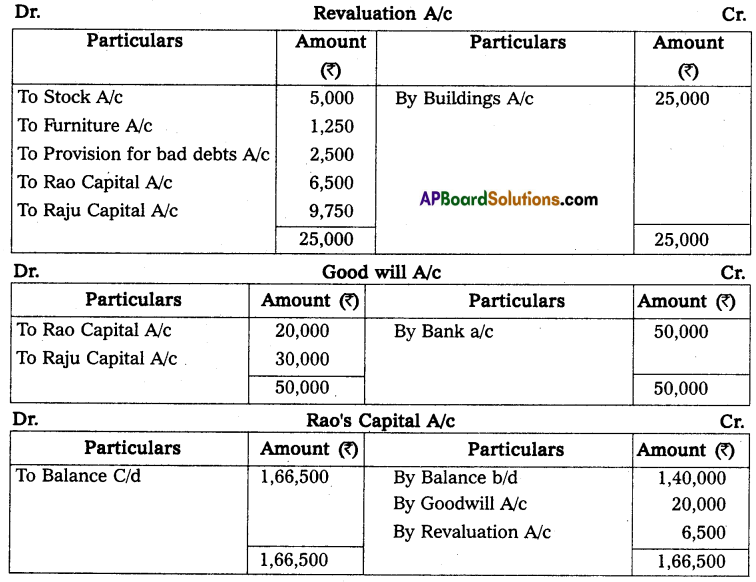

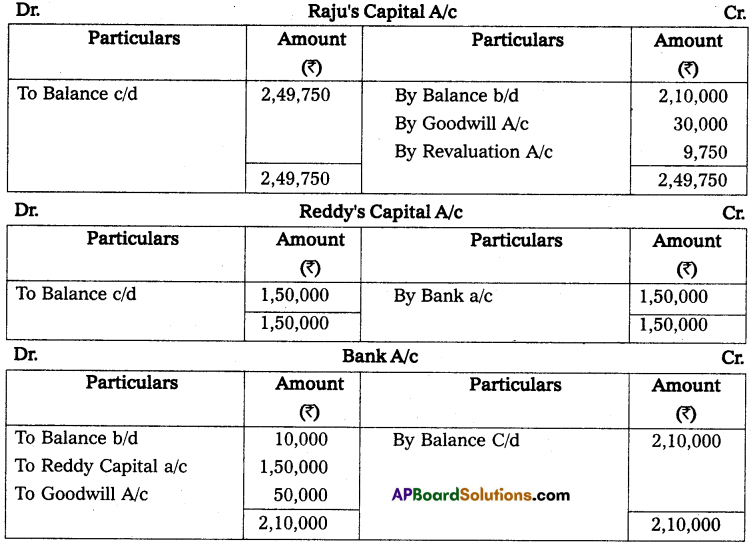

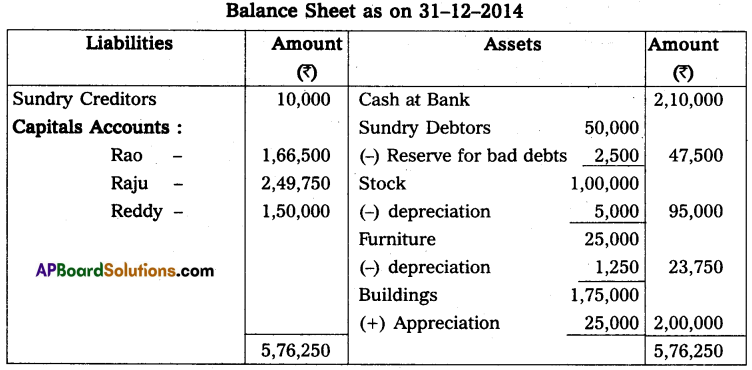

Rao and Raju are carrying on business in a partnership, sharing profit & loss in the ratio of 2 : 3. Their Balance sheet as of 31-12-2014 was as under.

On that day they admitted Reddy into partnership and gave him 1/6th share in the future profits on the following terms.

(a) Reddy is to bring in ₹ 1,50,000 as his capital and ₹ 50,000 as goodwill, which sum is to remain in the business.

(b) Stock and furniture are to be reduced in value by 5%.

(c) Buildings are to be appreciated by ₹ 25,000.

(d) A provision of 5% to be created on sundry debtor for doubtful debts.

Write Journal entries to record the above arrangement and show the opening Balance sheet of the new firm.

Solution:

![]()

Question 19.

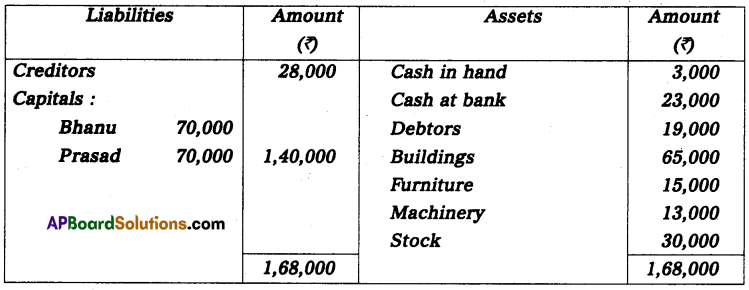

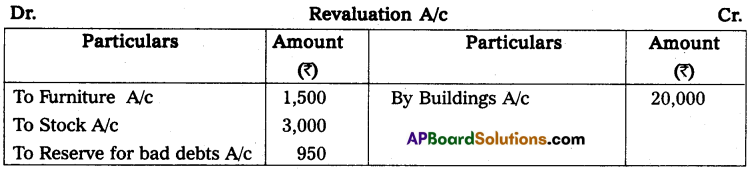

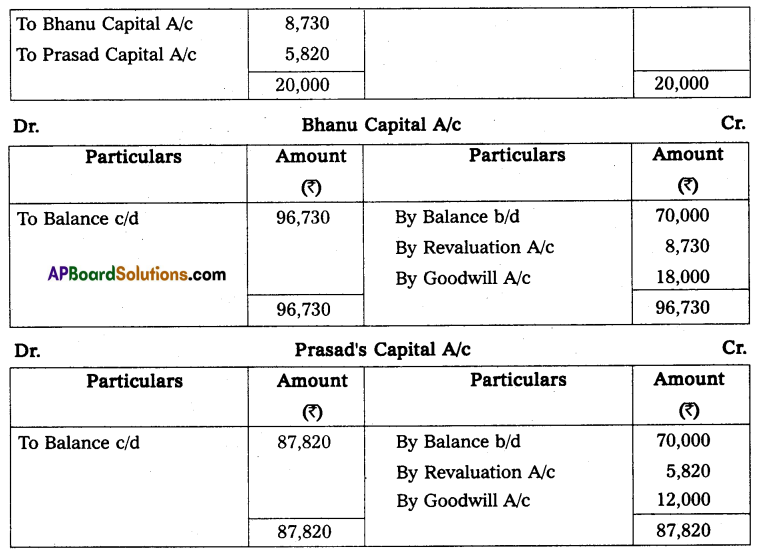

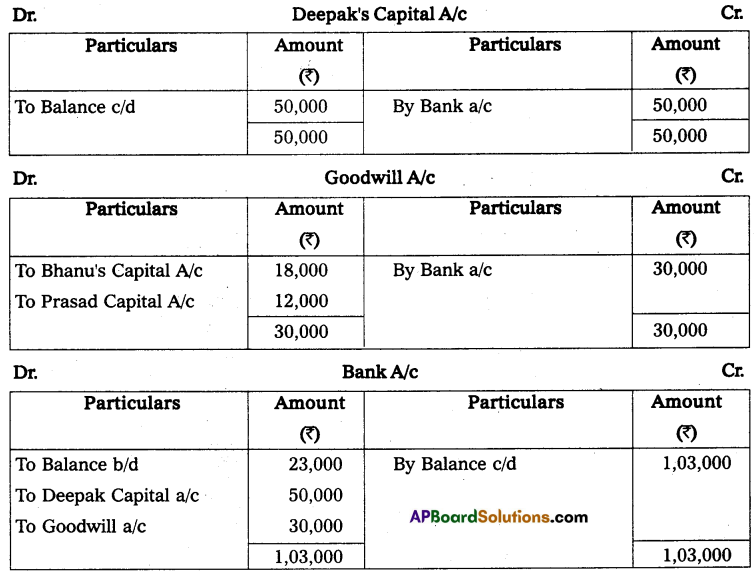

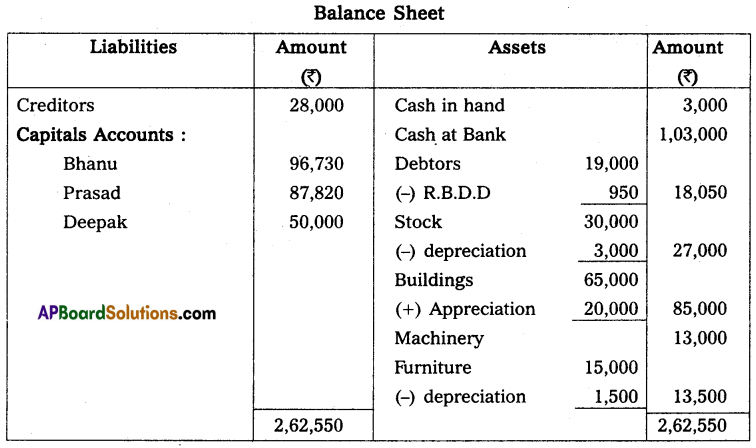

Bhanu and Prasad are partners sharing profit and losses in the ratio of 3 : 2 respectively. Their Balance Sheet as on March 31, 2015, was as under:

On that date they admit Deepak into a partnership for 1/3 share in future profit on the following terms:

(i) Furniture and stock are to be depreciated by 10%.

(ii) Building is appreciated by ₹ 20,000.

(iii) 5% provision is to be created on Debtors for doubtful debts.

(iv) Deepak is to bring in ₹ 50,000 as his capital and ₹ 30,000 as goodwill.

Make necessary Ledger Account and Balance Sheet of the new firm.

Solution:

Question 20.

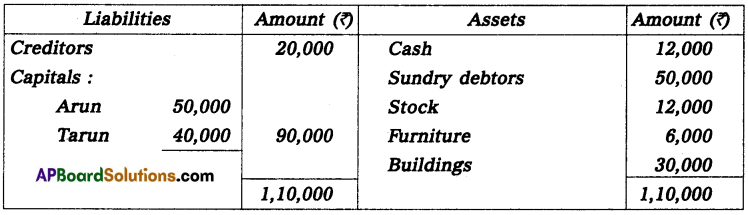

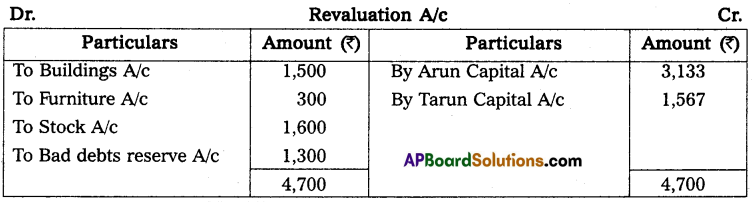

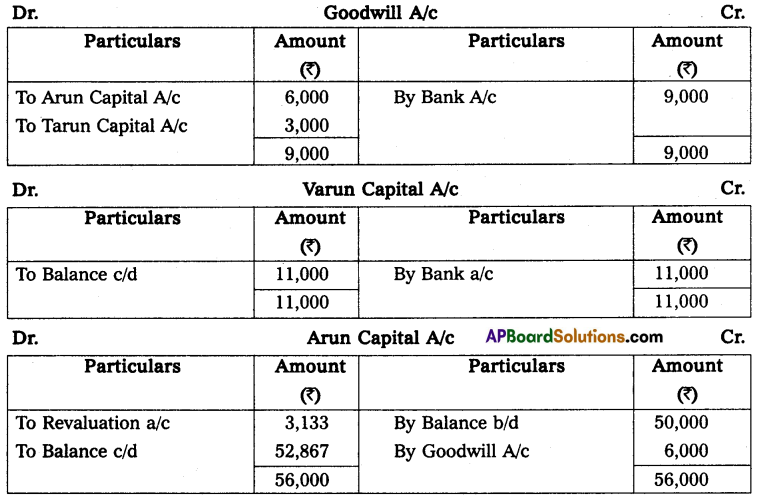

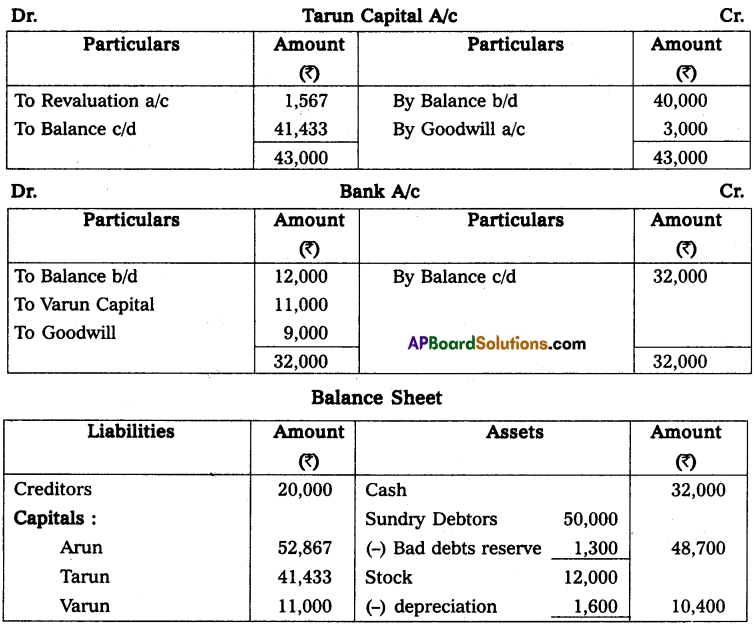

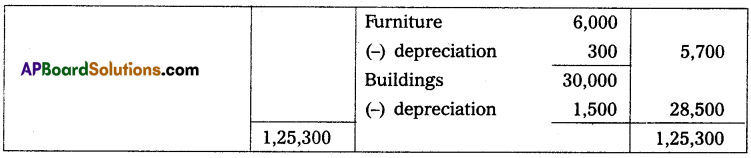

The following is the Balance sheet of Arun and Tarun sharing profit and losses in the ratio of 2 : 1.

They agreed to admit Vanin into partnership on the following terms:

(i) Varun to pay ₹ 9,000 as Goodwill.

(ii) Varun brings ₹ 11,000 as Capital for 1/4 share of profit in the business.

(iii) Budding and furniture to be depreciated at 5%. Stock is reduced by ₹ 1,600 and Bad Debt Reserve ₹ 1,300 to be provided for.

Prepare necessary ledger accounts and balance sheets after admission.

Solution:

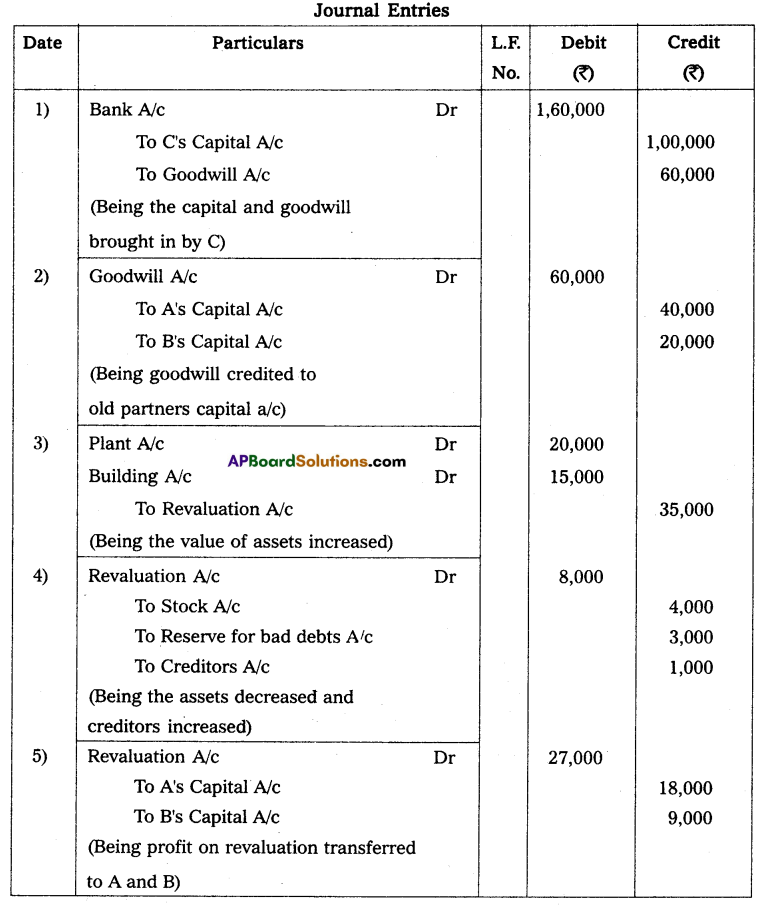

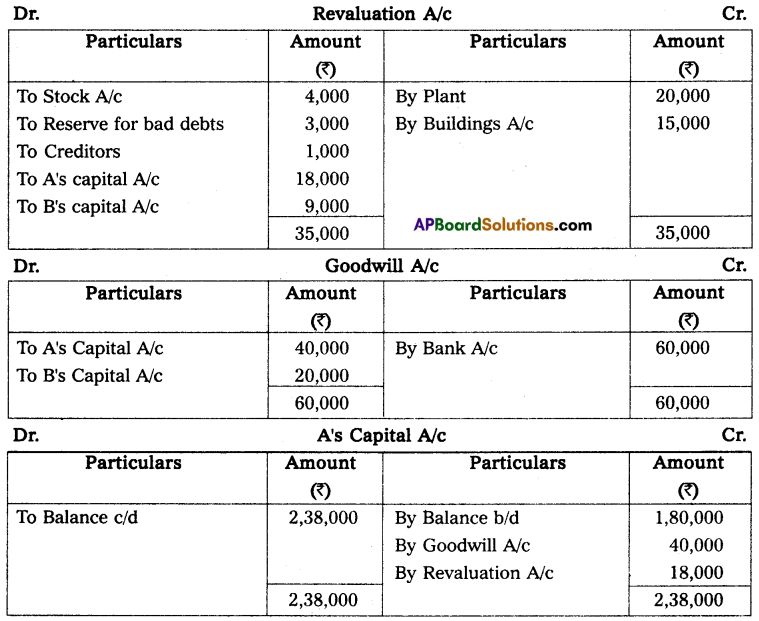

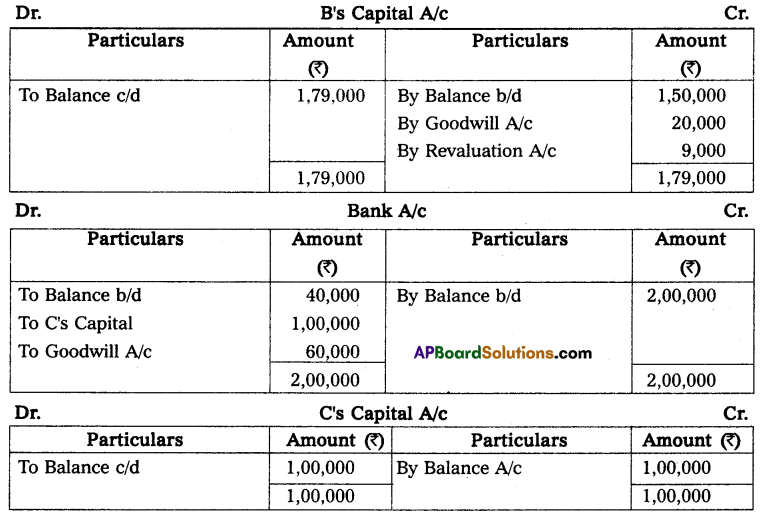

Question 21.

A and B are partners in the firm sharing profits in the ratio 2 : 1. C is admitted into the firm with 1/4 share in profits. He will bring in ₹ 30,000 as capital and the capitals of A and B are to be adjusted in the profit sharing ratio. The Balance Sheet of A and B as on March 31, 2014 (before C’s admission) was as under:

Other terms of the agreement are as under:

1. C will bring in ₹ 12,000 as his share of goodwill.

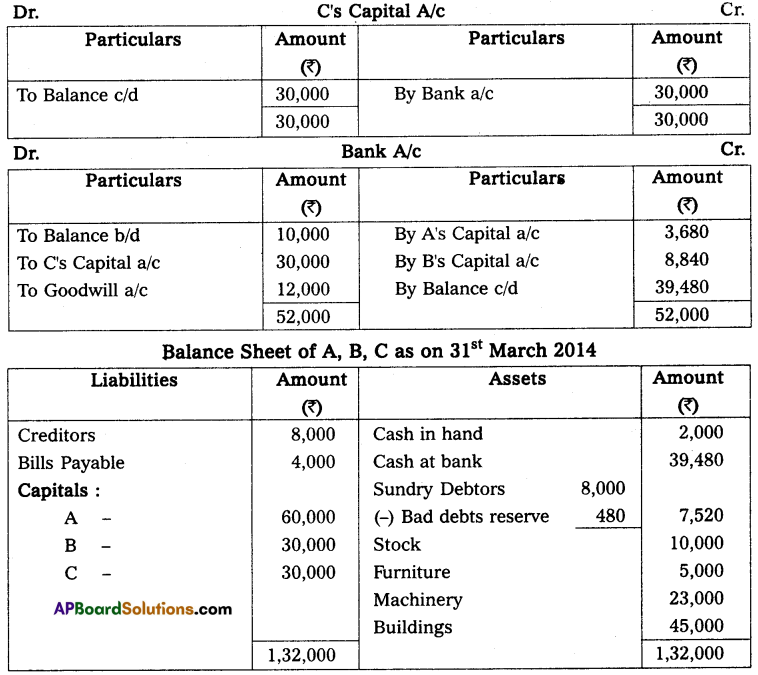

2. Building was valued at ₹ 45,000 and Machinery at ₹ 23,000

3. A provision for bad debts is to be created @ 6% on debtors.

4. The capital accounts of A and B are to adjust.

Record necessary journal entries, show necessary ledger accounts, and prepare a Balance Sheet after C’s admission.

Solution:

Calculation of New profit sharing ratio:

C’s share = \(\frac{1}{4}\)

Remaining share = 1 – \(\frac{1}{4}\) = \(\frac{3}{4}\)

Old ratio = \(\frac{2}{3}: \frac{1}{3}\)

New profit sharing ratio

A = \(\frac{2}{3} \times \frac{3}{4}=\frac{6}{12}\)

B = \(\frac{1}{3} \times \frac{3}{4}=\frac{3}{12}\)

C s share = \(\frac{1}{4} \text { or } \frac{3}{12}\)

A’s Capital = \(\frac{2}{4} \times \frac{4}{1} \times 30,000\) = 60,000

B’s Capital for \(\frac{1}{4}\) share = 30,000

![]()

Question 22.

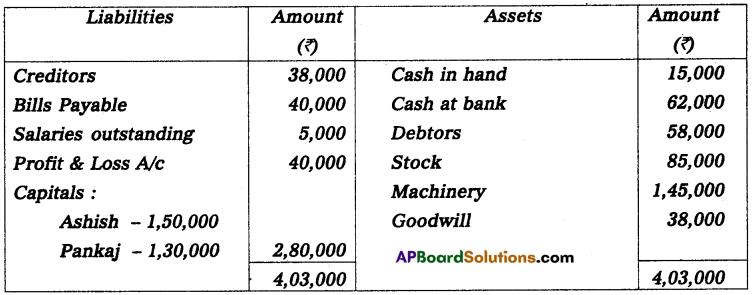

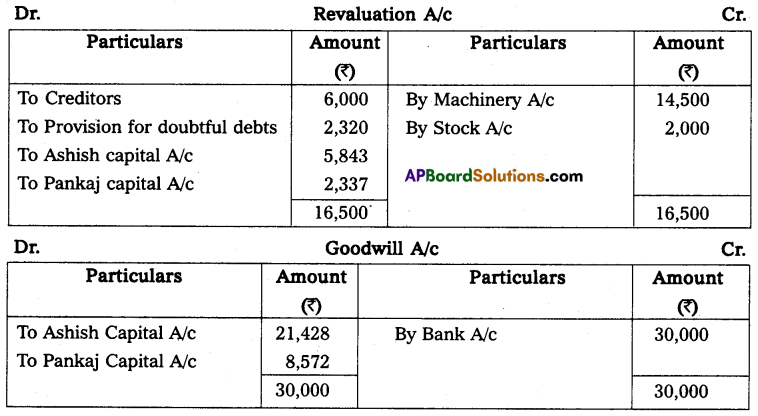

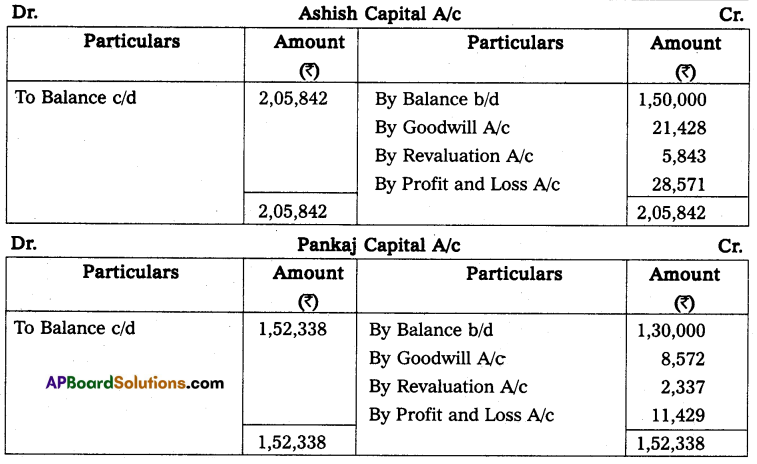

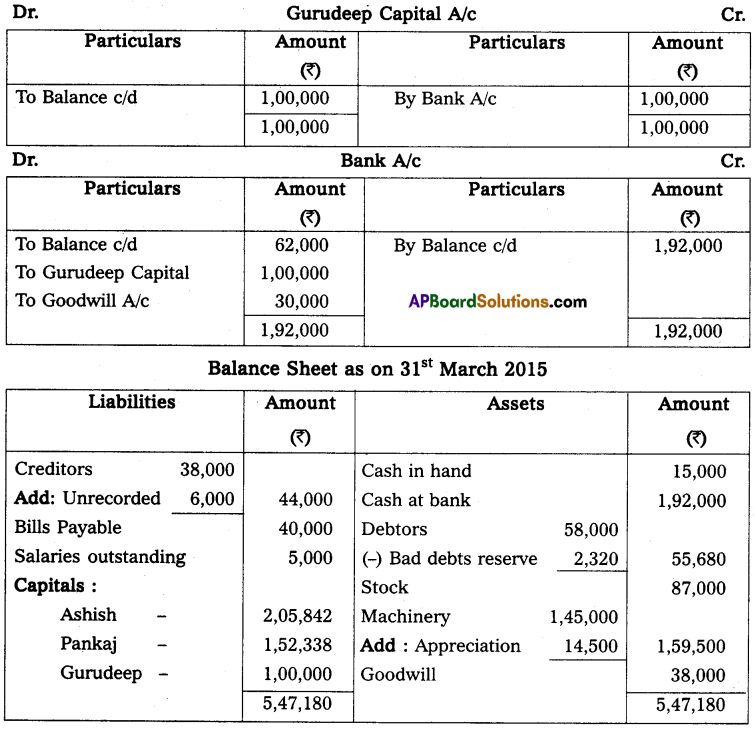

Ashish and Pankaj are partners sharing profit in the ratio of 5 : 2, their Balance sheet on March 31, 2015, was as follows:

They admitted Gurudeep into partnership on the following terms on March 31, 2015.

(a) New profit sharing ratio is agreed upon as 3 : 2 : 1.

(b) He will bring in ₹ 1,00,000 as his shared capital and ₹ 30,000 as his share of goodwill.

(c) Machinery is appreciated by 10%

(d) Stock is valued at ₹ 87,000.

(e) Creditors are unrecorded to the extent of ₹ 6,000

(f) A provision for doubtful debts is to be created by 4% on debtors.

Prepare the Revaluation account, Capital Accounts, Bank account, and Balance Sheet of the new firm after the admission of Gurdeep.

Solution:

Question 23.

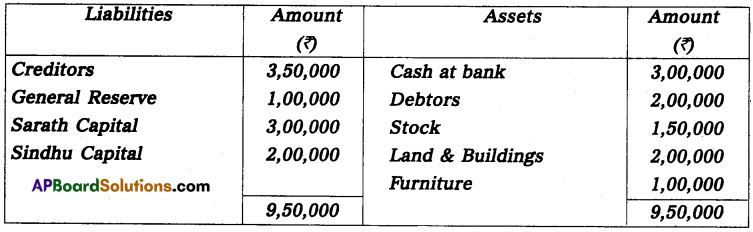

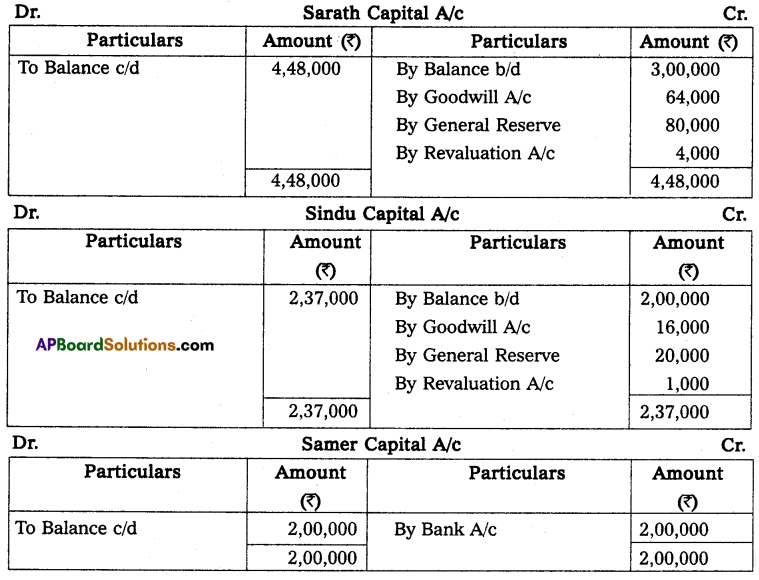

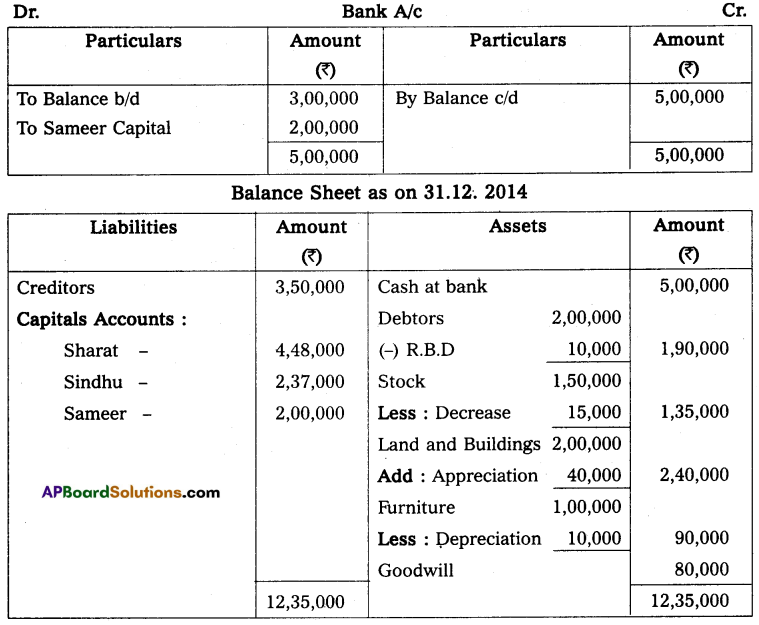

The Balance Sheet of Sarath and Sindhu as of 31.12.2014 who are sharing profits and losses in the ratio of 4 : 1 is as follows:

They have agreed to admit Sameer under the following conditions:

(a) Sameer has to bring the capital of ₹ 2,00,000 for his 1/5th share of profits.

(b) Furniture and stock have to be depreciated by 10% and a reserve of 5% have to be created on debtors for bad and doubtful debts.

(c) Land and Buildings have to be appreciated by 20%.

(d) Goodwill has to be raised by ₹ 80,000.

Prepare necessary ledger A/c and the balance sheet of the new firm.

Solution:

Question 24.

Given below is the Balance Sheet of A and B, who are carrying on partnership business on 31.12.2014. A and B are sharing profits and losses in the ratio of 2 : 1.

C is admitted as a partner on the date of the balance sheet on the following terms:

(i) C will bring in ₹ 1,00,000 as his capital and ₹ 60,000 as his share of goodwill for 1/4 share in the profits.

(ii) Plant is to be appreciated to ₹ 1,20,000 and the value of buildings is to be appreciated by 10%.

(iii) Stock is found overvalued by ₹ 4,000.

(iv) A provision for bad and doubtful debts is to be created at 5% of debtors.

(v) Creditors were unrecorded to the extent of ₹ 1,000.

Pass the necessary journal entries, prepare the revaluation account and partners’ capital accounts, and show the Balance Sheet after the admission of C.

Solution:

![]()

Question 25.

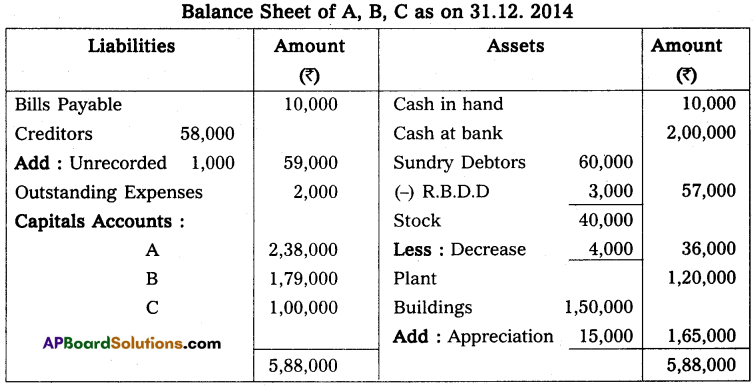

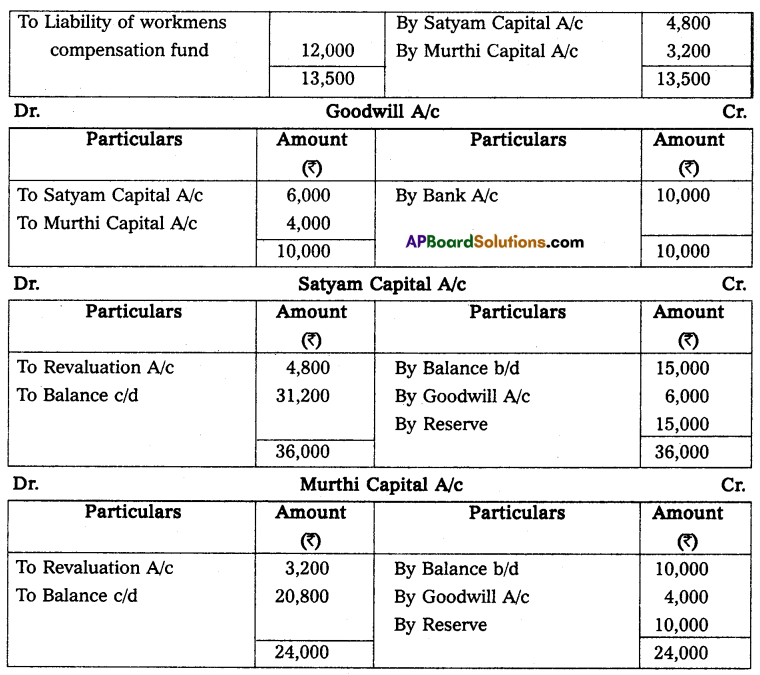

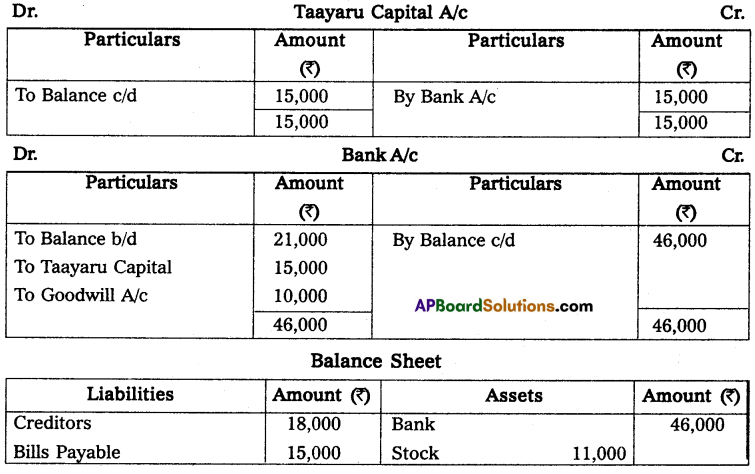

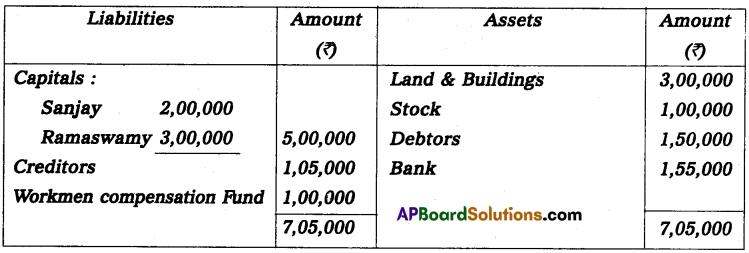

Following is the Balance Sheet of Satyam and Murthi sharing profit as 3 : 2.

On admission of Tayaru for 1/6th share in the profit, it was decided that:

(i) Provision for doubtful debts to be increased by 1,500.

(ii) Value of land and buildings to be increased to 21,000.

(iii) Value of stock to be increased by 2,500.

(iv) The liability of the workmen’s compensation fund was determined to be 12,000.

(v) Tayaru brought in as her share of goodwill 10,000 in cash.

(vi) Tayaru was to bring further cash of 15,000 for her capital.

Prepare Revaluation AJc, Capital A/c, and the Balance Sheet of the new firm.

Solution:

Question 26.

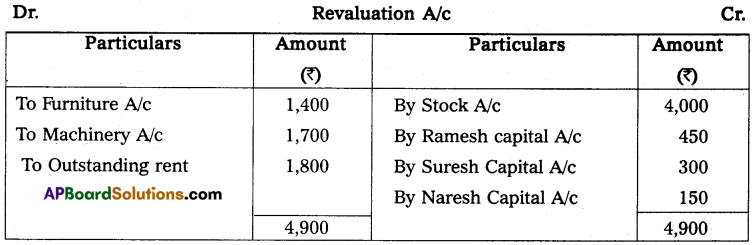

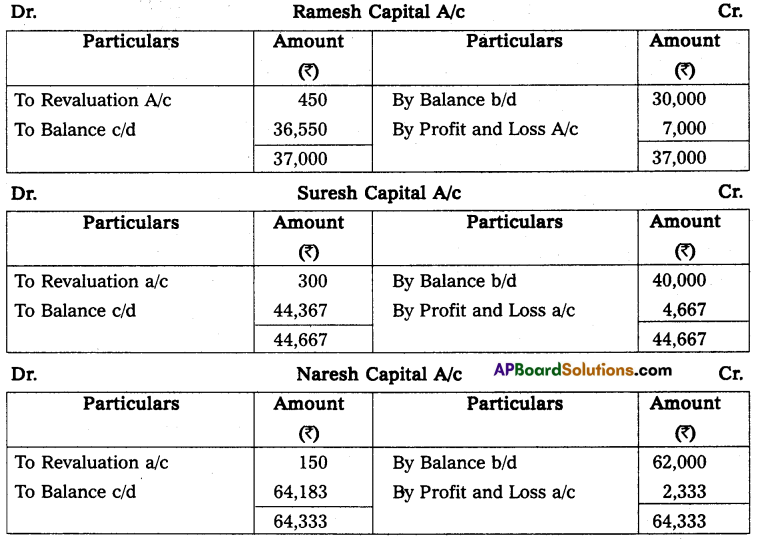

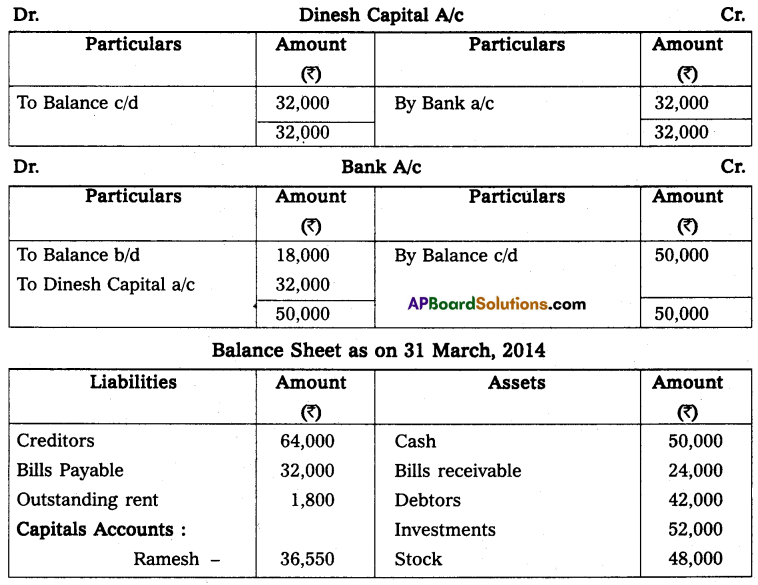

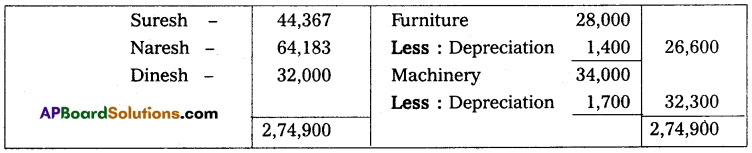

Ramesh, Suresh, and Naresh are partners sharing profits and losses in the ratio of 1 : 2 : 3. On 31st March 2014, their Balance Sheet was as follows;

They admit Dinesh into partnership on the following terms:

(i) Furniture and Machinery to be depreciated by 5%.

(ii) Stock is evaluated at 48,000.

(iii) Outstanding rent amount to 1,880

(iv) Dinesh to bring 32,000 towards his capital for 1/6th share.

Prepare the Revaluation Account, Partners Capital Accounts, and Balance Sheet of the new firm.

Solution:

Question 27.

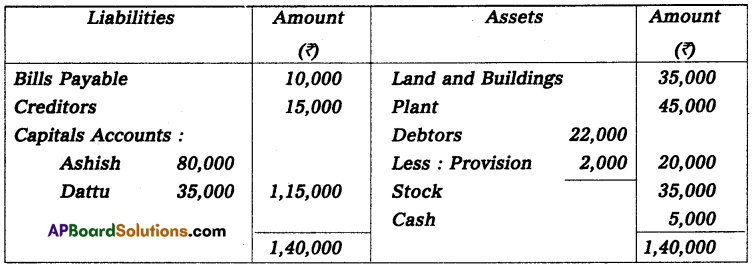

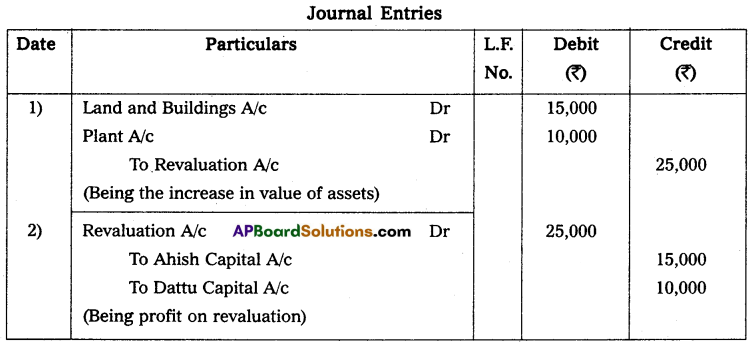

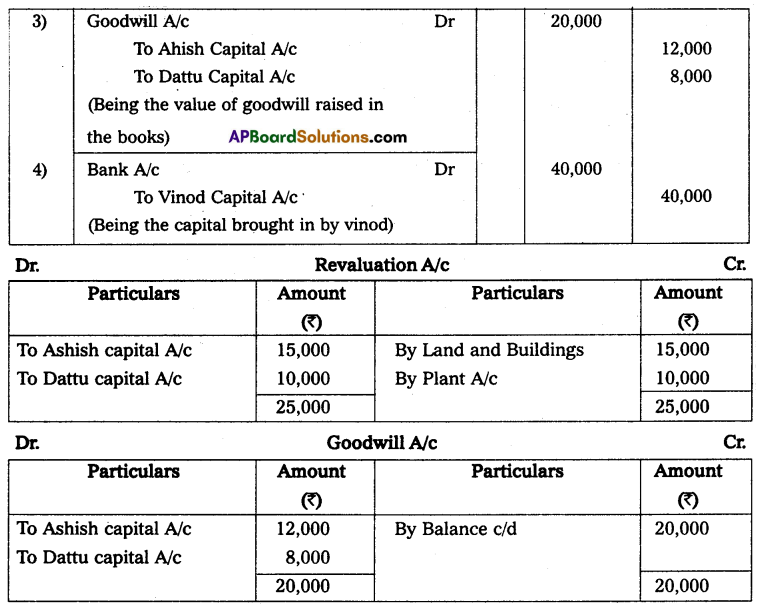

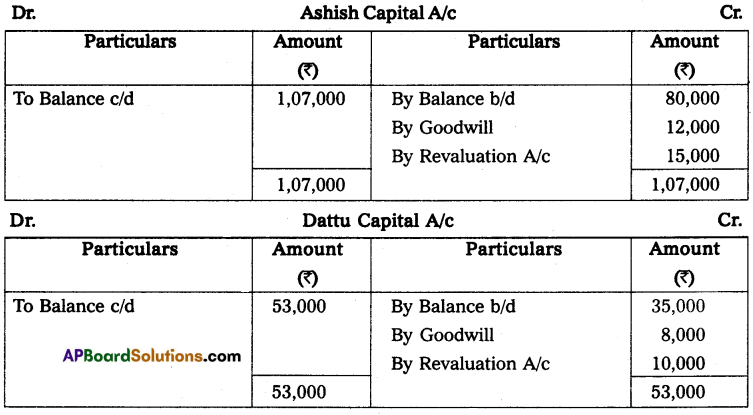

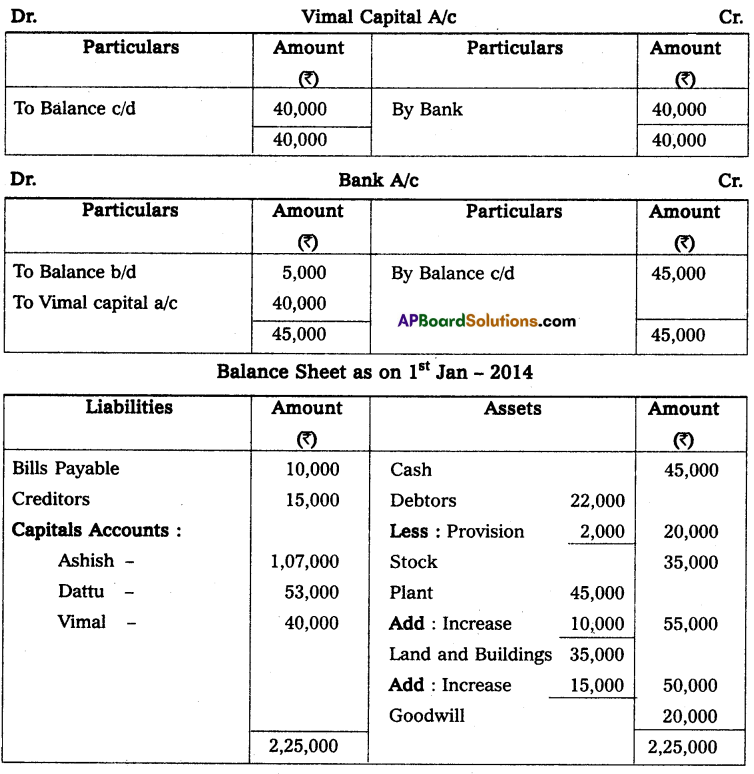

Ashish and Dattu were partners in the firm sharing profits in 3 : 2 ratio. On Jan 01, 2014, they admitted Vimal for 1/5 share in the profits. The Balance Sheet of Ashish and Dattu as on Jan. 01, 2014, was as follows:

It was agreed that:

(i) The value of Land and Buildings be increased by ₹ 15,000.

(ii) The value of the plant be increased by ₹ 10,000.

(iii) Goodwill of the firm be valued at ₹ 20,000

(iv) Vimal to bring in capital to the extent of 1/5th of the total capital of the new firm.

Record the necessary journal entries and prepare the Balance Sheet of the firm after Vimal’s admission.

Solution:

Note: Vimal is given a share of \(\frac{1}{5}\).

The remaining share is 1 – \(\frac{1}{5}\) = \(\frac{4}{5}\)

The total capitals of Ashish and Dattu after adjustments for \(\frac{4}{5}\) share = 1,60,000 (1,07,000 + 53,000)

The capital to be brought by Vimal for \(\frac{1}{5}\) share = \(\frac{1}{5} \times \frac{5}{4} \times 1,60,000\) = ₹ 40,000

![]()

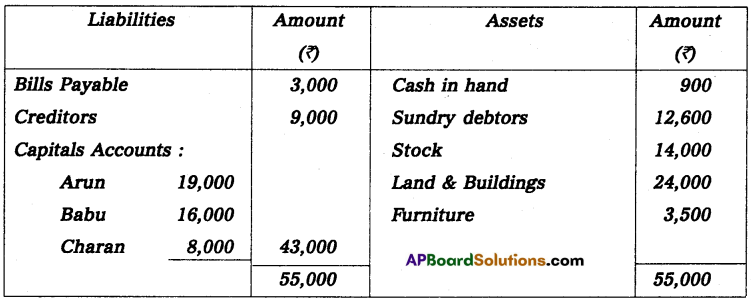

Question 28.

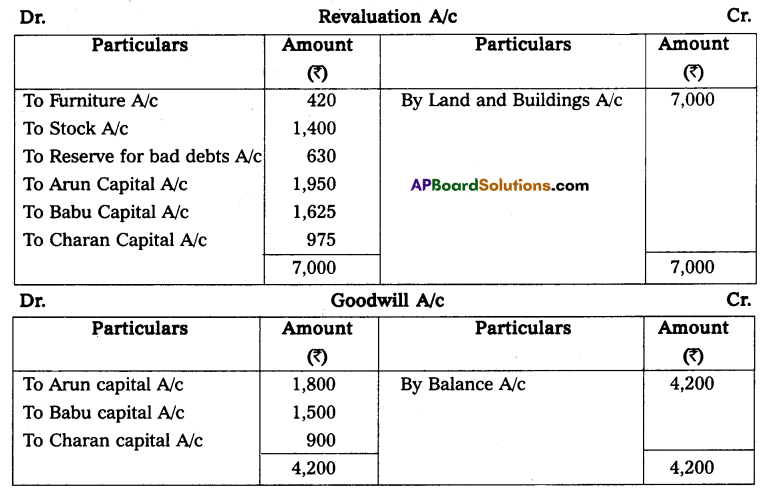

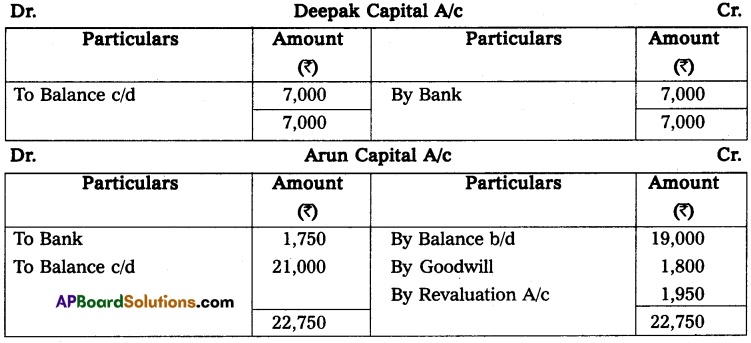

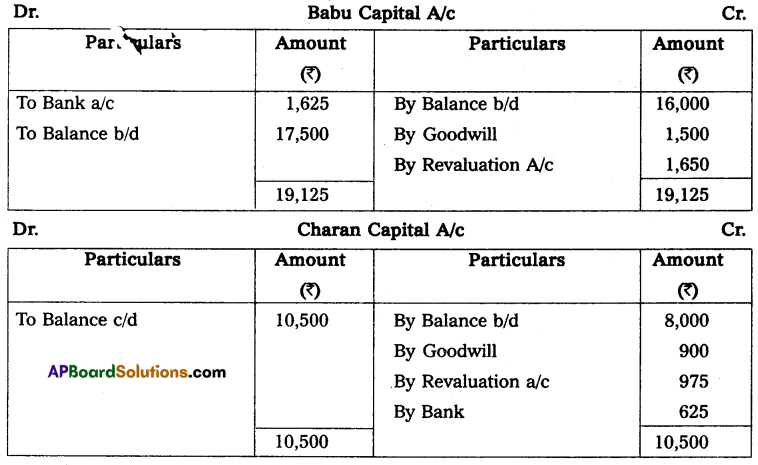

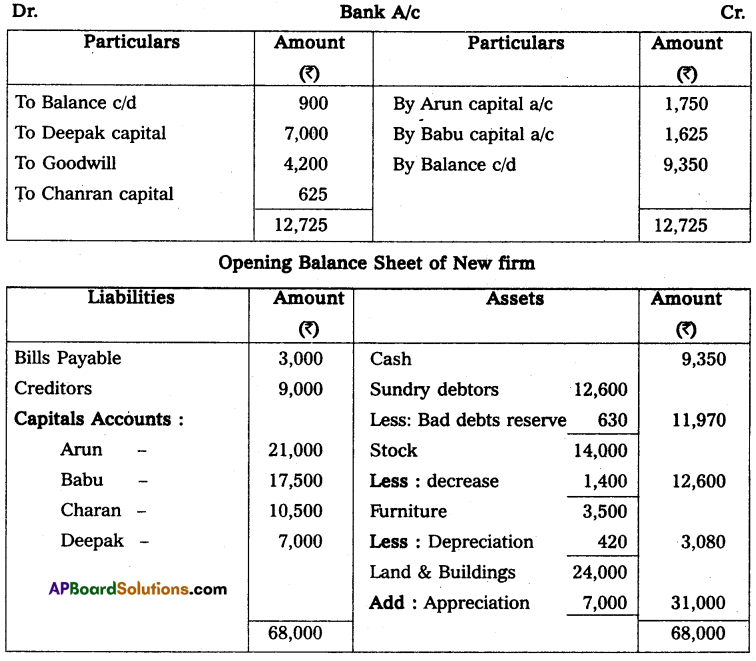

The following was the Balance Sheet of Arun, Bhanu, and Charan sharing profits and losses in the ratio of 6 : 5 : 3 respectively.

They agreed to take Deepak into partnership and give him a share of 1/8 on the following terms:

(a) that Deepak should bring in ₹ 4,200 as goodwill and ₹ 7,000 as his Capital;

(b) that furniture be depreciated by 12%;

(c) that stock be depreciated by 10%;

(d) that a Reserve of 5% be created for doubtful debts;

(e) that the value of land and buildings having appreciated being brought upto ₹ 31,000;

(f) that after making the adjustments the capital accounts of the old partners be adjusted on the basis of the proportion of Deepak’s Capital to his share in the business, i.e., actual cash to be paid off, or brought in by the old partners as the case may be.

Prepare Necessary Accounts and the Opening Balance Sheet of the new firm.

Solution:

Old profit sharing ratio = \(\frac{6}{14}: \frac{5}{14}: \frac{3}{14}\)

Share given to Deepak = \(\frac{1}{8}\)

Remaining share = 1 – \(\frac{1}{8}\) = \(\frac{7}{8}\)

New profit sharing ratio

Arun = \(\frac{7}{8} \times \frac{6}{14}=\frac{42}{112}\)

Babu = \(\frac{7}{8} \times \frac{5}{14}=\frac{35}{112}\)

Charan = \(\frac{7}{8} \times \frac{3}{14}=\frac{21}{112}\)

Deepak = \(\frac{1}{8} \text { or } \frac{14}{112}\)

Total Ratio = 6 : 5 : 3 : 2

Arun capital = \(\frac{6}{16} \times \frac{16}{2} \times 7000\) = 21,000

Babu capital = \(\frac{5}{16} \times \frac{16}{2} \times 7000\) = 17,500

Charan capital = \(\frac{3}{16} \times \frac{16}{2} \times 7000\) = 10,500

Textual Examples

Case 1: If the new partner share is given along with the old ratio

Question 1.

Anil and Vishal are partners sharing profits in the ratio of 3 : 2. They admitted Sumit as a new partner for 1/5 share in the future profits of the firm. Calculate the new profit sharing ratio of Anil, Vishal, and Sumit.

Solution:

If we assume the total share is 1

The new partner sumit’s share = \(\frac{1}{5}\) share out of 1

Rest of the share = 1 – \(\frac{1}{5}\) = \(\frac{4}{5}\)

Old Ratio = 3 : 2

New Share = Rest of the share × old share

Anil’s new share = \(\frac{4}{5} \times \frac{3}{5}=\frac{12}{25}\)

Vishal’s new share = \(\frac{4}{5} \times \frac{2}{5}=\frac{8}{25}\)

New Ratio = \(\frac{12}{25}: \frac{8}{25}: \frac{1}{5}\)

New profit sharing ratio of Anil, Vishal, and Sumit = 12 : 8 : 5

Case 2: If the new partner gets his share equally from the old partner

Question 2.

Akshay and Bharat are partners sharing profits in the ratio of 3 : 2. They admit Dinesh as a new partner for 1/5th share in the future profits of the firm which he gets equally from Akshay and Bharat. Calculate the new profit-sharing ratio of Akshay, Bharat, and Dinesh.

Solution:

New partner Dinesh’s share = \(\frac{1}{5}\)

This is shared equally between Akshay and Bharat,

i.e., 1/2 of the Dinesh share = \(\frac{1}{5} \times \frac{1}{2}\) = \(\frac{1}{10}\) from each partner.

Old Ratio = 3 : 2

New share = Old share – Sacrificing share

Akshay’s new share = \(\frac{3}{5}-\frac{1}{10}=\frac{5}{10}\)

Bharat’s new share = \(\frac{2}{5}-\frac{1}{10}=\frac{3}{10}\)

New Ratio = \(\frac{5}{10}: \frac{3}{10}: \frac{1}{5}\)

The new profit sharing ratio among Akshay, Bharat, and Dinesh will be 5 : 3 : 2

Case 3: If the profit share of a new partner takes a particular ratio from the old partner

Question 3.

Anusha and Nitu are partners sharing profits in the ratio of 3 : 2. They admitted Jyoti as a new partner for 3/10 shares, which she acquired 2/10 from Anusha and 1/10 from Nitu. Calculate the new profit-sharing ratio of Anusha, Nitu, and Jyoti.

Solution:

New partner Jyoti’s share = \(\frac{3}{10}\) (this acquired 2/10 from Anusha and 1/10 from Nitu)

Old Ratio = 3 : 2

New share = Old share – Sacrificing share

Anusha’s new share = \(\frac{3}{5}-\frac{2}{10}=\frac{4}{10}\)

Nitu’s new share = \(\frac{2}{5}-\frac{1}{10}=\frac{3}{10}\)

The new ratio = \(\frac{4}{10}: \frac{3}{10}: \frac{3}{10}\)

The new profit sharing ratio among Anusha, Nitu, and Jyoti will be 4 : 3 : 3.

![]()

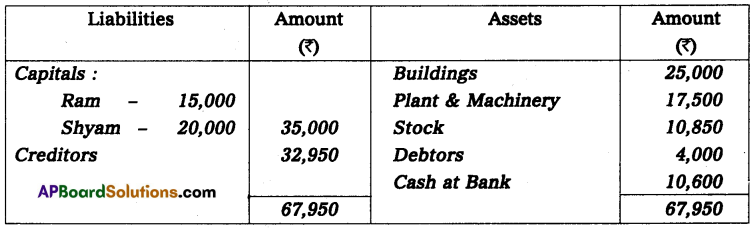

Case 4: If the old partners sacrifice a particular proportion of their shares to a new partner

Question 4.

Ram and Shyam are partners in firm sharing profits in the ratio of 3 : 2. They admit Ganesh as a new partner. Ram surrenders 1/4 of his share and Shyam 1/3 of his share in favour of Ganesh. Calculate the new profit-sharing ratio of Ram, Shyam, and Ganesh.

Solution:

New partner Ganesh’s profit share = 1/4 of Ram’s share + 1/3 of Shyam’s share

= \(\frac{3}{5} \times \frac{1}{4}+\frac{2}{5} \times \frac{1}{3}\)

= \(\frac{3}{20}+\frac{2}{15}\)

= \(\frac{17}{60}\)

Old Ratio = 3 : 2

Ram’s new share = Old Share – Scarifying Share

= \(\frac{3}{5}-\frac{3}{20}\)

= \(\frac{9}{20}\)

Shyam’s new share = \(\frac{2}{5}-\frac{2}{15}\)

= \(\frac{4}{15}\)

New ratio = \(\frac{9}{20}: \frac{4}{15}: \frac{17}{60}\)

The new profit sharing ratio among Ram, Shyam, and Ganesh will be 27 : 16 : 17

Case 5: If the new partner share takes entire from one partner

Question 5.

Das and Sinha are partners in the firm sharing profits in 3 : 2 ratio. They admitted Pal as a new partner for 1/4 share in the profits, which he acquired wholly from Das. Determine the new profit-sharing ratio of the partners.

Solution:

New partner Pal’s share = \(\frac{1}{4}\)

Das’s new share = \(\frac{3}{5}-\frac{1}{4}=\frac{7}{20}\)

Sinha’s old and new share = \(\frac{2}{5}\)

New ratio = \(\frac{7}{20}: \frac{2}{5}: \frac{1}{4}\)

The new profit sharing ratio among Das, Sinha, and Pal will be 7 : 8 : 5

Question 6.

Rohit and Mohit are partners in firm sharing profits in the ratio of 5:3. They admit Sarma as a new partner for 1/7 share in the profit. The new profit sharing ratio will be 4 : 2 : 1. Calculate the sacrificing ratio of Rohit and Mohit.

Solution:

Rohit and Mohits’s old Ratio = 5 : 3

Rohit, Mohit, and Sarmas’ New Ratio = 4 : 2 : 1

Rohit’s old share = \(\frac{5}{8}\)

Rohit’s new share = \(\frac{4}{7}\)

Sacrifice share = Old Share of Profit – New Share of Profit

Rohit’s sacrifice share = \(\frac{5}{8}-\frac{4}{7}=\frac{3}{56}\)

Mohit’s old share = \(\frac{3}{8}\)

Mohit’s new share = \(\frac{2}{7}\)

Mohit’s sacrifice share = \(\frac{3}{8}-\frac{2}{7}=\frac{5}{56}\)

Sacrificing ratio = \(\frac{3}{56}: \frac{5}{56}\)

Sacrificing ratio of Rohit and Mohit will be 3 : 5

Note: The old partner’s sacrificing ratio is equal to the old ratio if the new partner’s share is given along with the old ratio (i.e. case – I).

Question 7.

R and S are partners, sharing profits in the ratio of 1 : 2. T admits for 1/5 share. State the sacrificing ratio.

Solution:

If we assume the total share is 1

The new partner T’s share = \(\frac{1}{5}\) share out of 1

Rest of the share = 1 – \(\frac{1}{5}\) = \(\frac{4}{5}\)

Old Ratio = 1 : 2

New Share = Rest of the share × old share

R’s new share = \(\frac{4}{5} \times \frac{1}{3}=\frac{4}{15}\)

S’ s new share = \(\frac{4}{5} \times \frac{2}{3}=\frac{8}{15}\)

Sacrifice share = Old Share of Profit – New Share of Profit

R’s sacrificing share = \(\frac{1}{3}-\frac{4}{15}=\frac{1}{15}\)

S’s sacrificing share = \(\frac{2}{3}-\frac{8}{15}=\frac{2}{15}\)

Sacrificing Ratio = \(\frac{1}{15}: \frac{2}{15}\)

Sacrificing ratio of R and S = 1 : 2

![]()

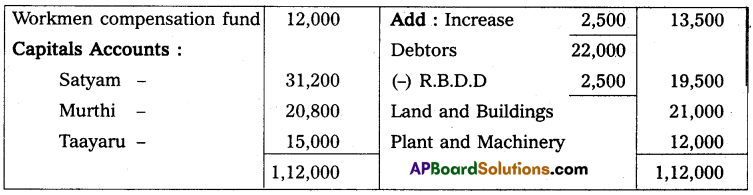

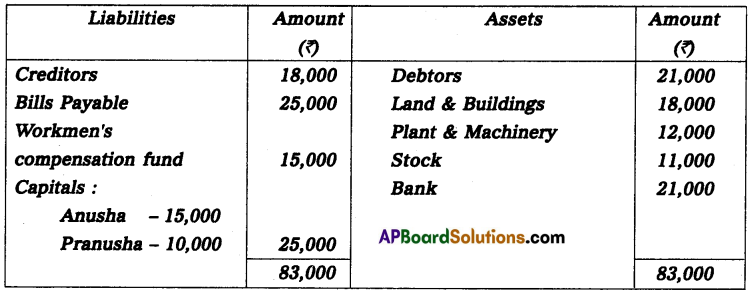

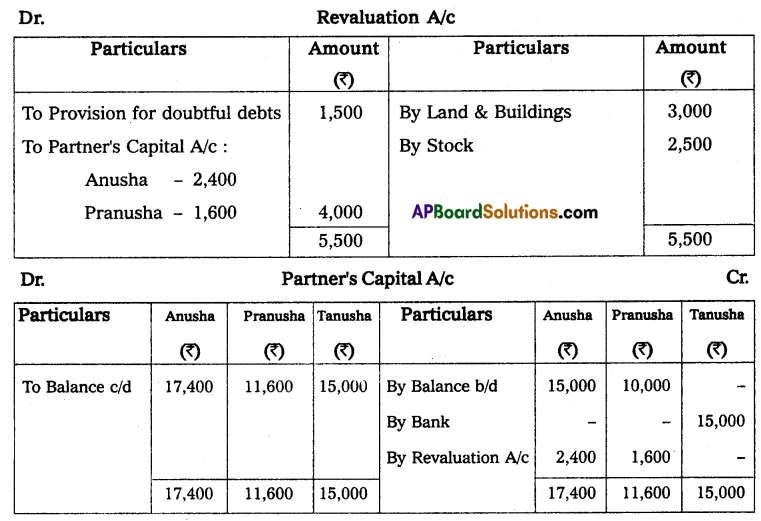

Question 8.

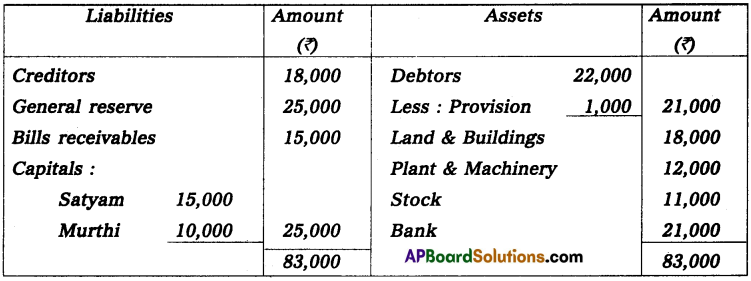

Following is the Balance Sheet of Anusha and Pranusha sharing profit as 3 : 2.

On admission of Tanusha for 1/6th share in the profit, it was decided that

(i) Provision for doubtful debts to be created by ₹ 1,500.

(ii) Value of land and building to be increased to ₹ 21,000.

(iii) Value of stock to be increased to ₹ 13,500.

(iv) Tanusha was to bring further cash of ₹ 15,000 for her capital.

Prepare Revaluation A/c and Capital Accounts.

Solution:

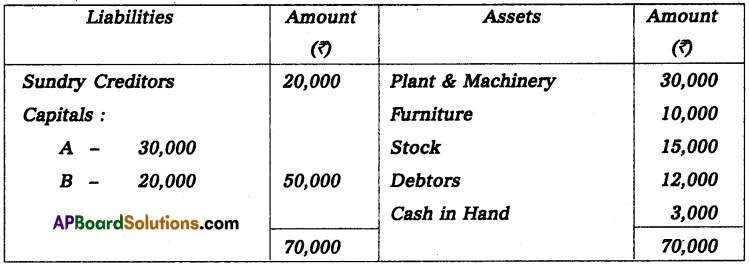

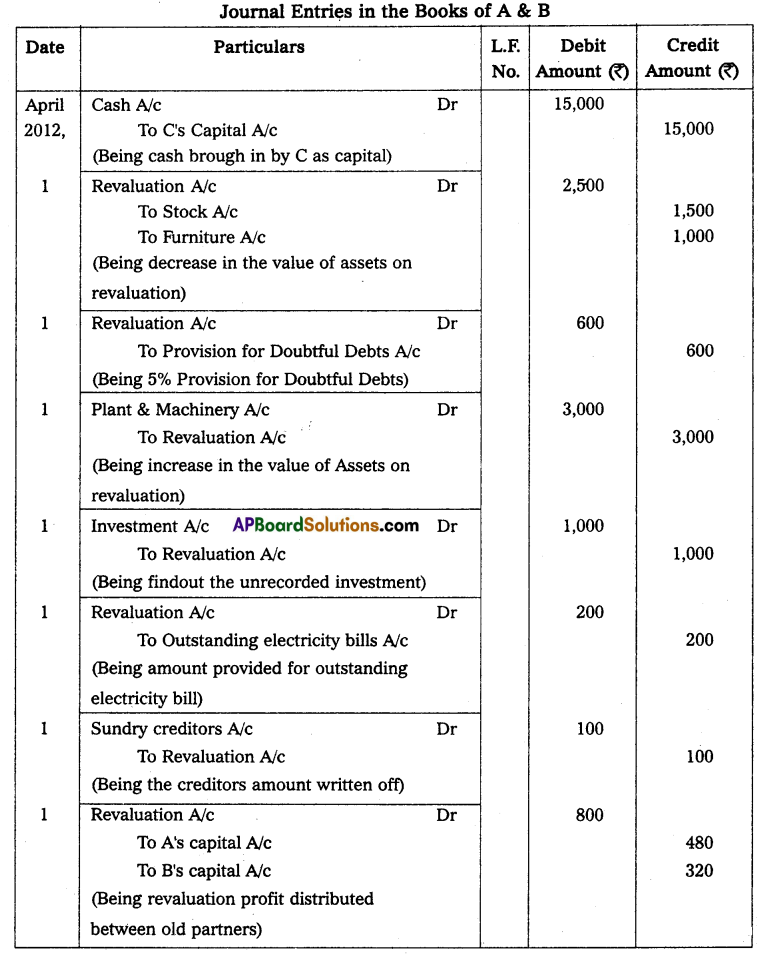

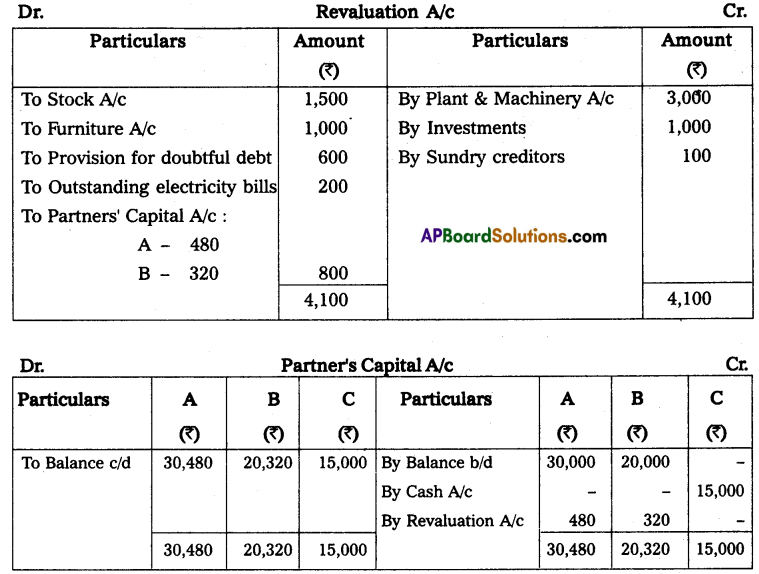

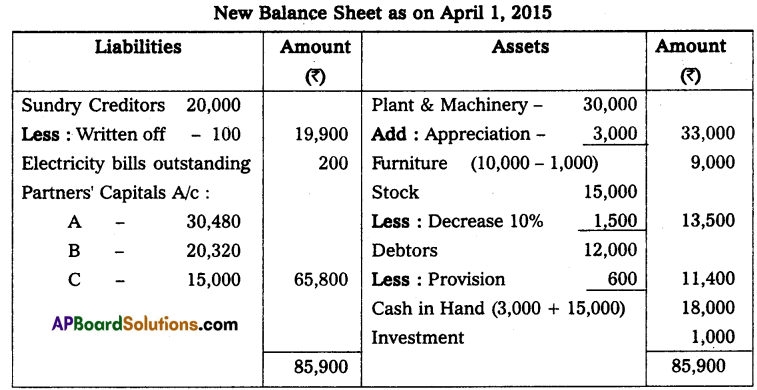

Question 9.

Following is the Balance Sheet of A and B who share profits in the ratio of 3 : 2.

Balance Sheet of A and B as on April 1, 2015

On that date C is admitted into the partnership on the following terms:

1. C is to bring in ₹ 15,000 as capital for 1/6 share.

2. The value of a stock is reduced by 10% while plant and machinery are appreciated by 10%.

3. Furniture is revalued at ₹ 9,000.

4. A provision for doubtful debts is to be created on sundry debtors at 5%.

5. Investment worth ₹ 1,000 and electricity bills outstanding ₹ 200 (not mentioned in the balance sheet) are to be taken into account.

6. A creditor of ₹ 100 is not likely to claim his money and is to be written off.

Record journal entries and prepare the Revaluation Account, Partners’ Capital Account, and New Balance Sheet of the firm.

Solution:

Question 10.

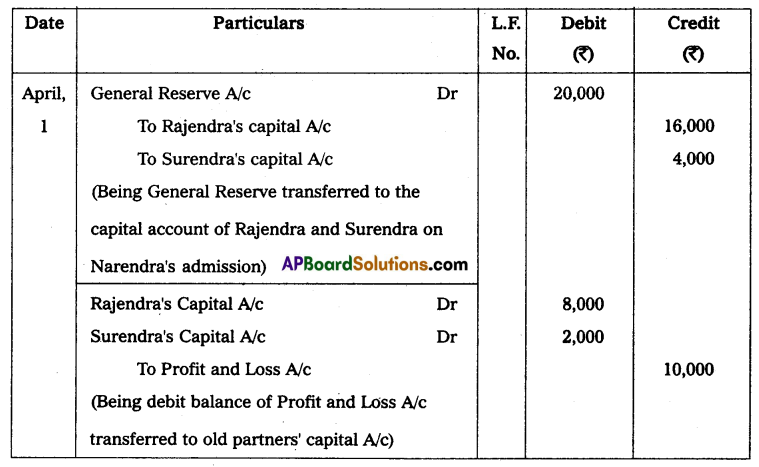

Rajendra and Surendra are partners in a firm sharing profits in the ratio of 4 : 1. On April 1, 2015, they admit Narendra as a new partner. On that date, there was a balance of ₹ 20,000 in general reserve and a debit balance (loss) of ₹ 10,000 in the profit and loss account of the firm. Pass necessary journal entries regarding adjustment of accumulated profit or loss.

Solution:

Journals in the Books of Rajendra, Surendra and Narendra

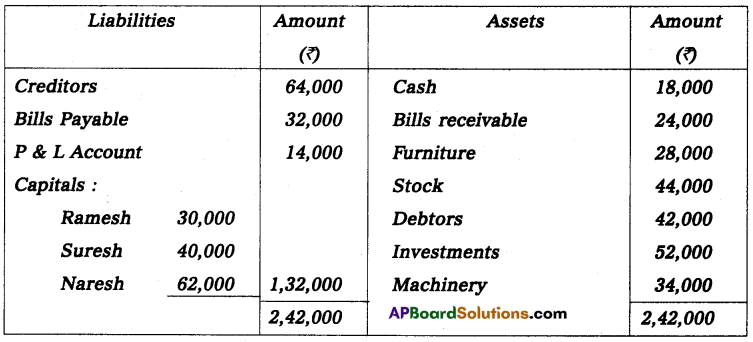

Question 11.

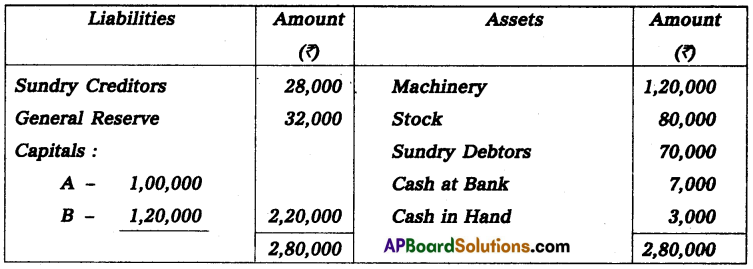

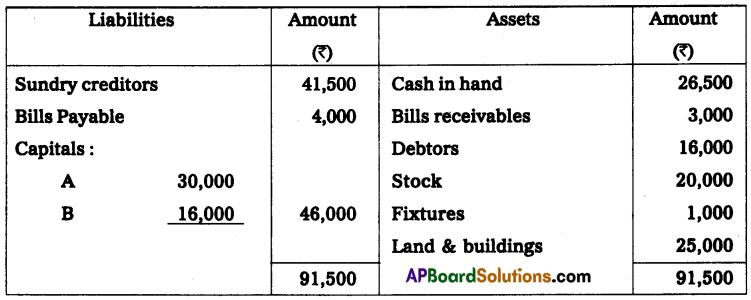

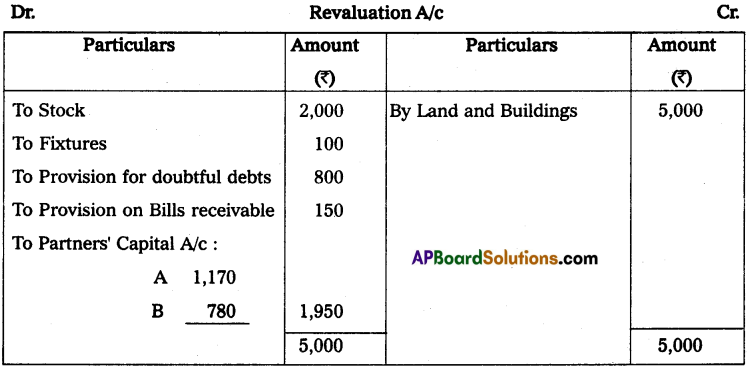

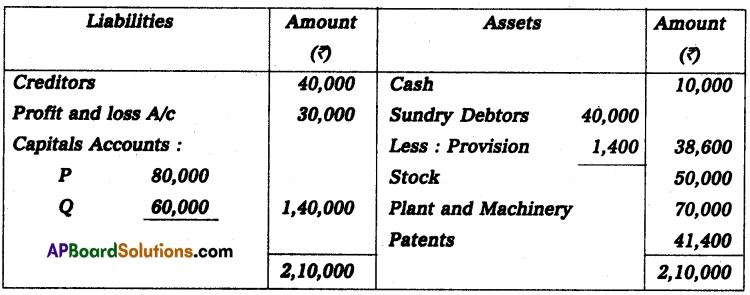

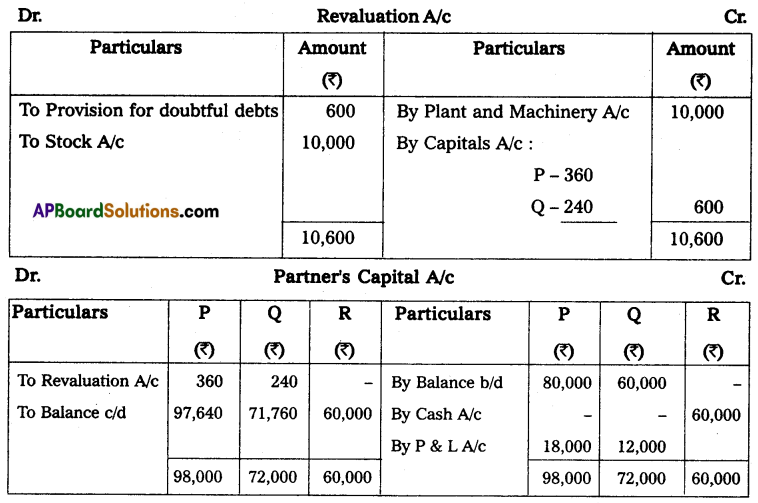

A & B are partners in a firm, sharing Profits and Loss in the ratio of 5 : 3. On 31 Dec 2014 their Balance Sheet was as under;

Balance Sheet as of 31st Dec 2014

On the above date they decided to admit C as a new partner on the following terms;

(a) A, B, and C’s new profit sharing ratio will be 7 : 5 : 4

(b) C will bring ₹ 1,00,000 as his capital.

(c) Machine is to be valued at ₹ 1,50,000, Stock ₹ 1,00,000, and a provision for the doubtful debt of ₹ 10,000 is to be created.

Prepare Revaluation A/c, Partners’ Capital A/C, and new Balance Sheet of the firm.

Solution:

![]()

Question 12.

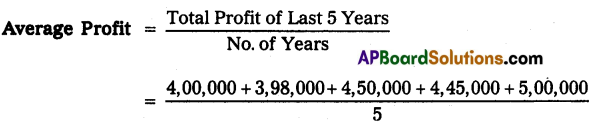

The profit for the five years of a firm are as follows – year 2009 ₹ 4,00,000; year 2010 ₹ 3,98,000; year 2011 ₹ 4,50,000; year 2012 ₹ 4,45,000 and year 2013 ₹ 5,00,000. Calculate goodwill of the firm on the basis of 4 years purchase of 5 years average profits.

Solution:

= \(\frac{21,93,000}{5}\)

= ₹ 4,38,600

Goodwill = Average Profit × No. of years’ purchase

= ₹ 4,38,600 × 4

= ₹ 17,54,400

2. Super Profit Method: Super Profit is the profit earned by the business that is in excess of the normal profit. Goodwill is determined by multiplying the super profit by the number of years’ purchase.

Normal Profit = Capital Employed × Normal Rate of Return /100.

Actual Profit = This is the profit earned by the firm during the year or it is also taken as the average of the last few years’ profit.

Super Profit = Actual Profit – Normal Profit.

Goodwill = Super Profit × No. of Years’ Purchase.

Question 13.

A firm earns a profit of ₹ 65,000 on a capital of ₹ 4,80,000 and the normal rate of return in a similar business is 10%. 3 years’ purchase value of super profit will be treated as goodwill.

Solution:

Normal Profit = Capital employed × Normal rate of return/100

= 4,80,000 × 10/100

= 48,000

Actual Profit = ₹ 65,000

Super Profit = Actual profit – Normal profit

= ₹ 65,000 – ₹ 48,000

= ₹ 17,000

Goodwill = Super Profit × No. of Years’ Purchase

= 17,000 × 3

= ₹ 51,000

Question 14.

A firm earned average profit during the last few years is ₹ 40,000 and the normal rate of return in a similar business is 10%. The total assets are ₹ 3,60,000 and outside liabilities are ₹ 50,000. Calculate the value of goodwill with the help of the Capitalisation of the Average profit method.

Solution:

Capital employed = Total assets – Outside liabilities

= ₹ 3,60,000 – ₹ 50,000

= ₹ 3,10,000

Capitalised value of average profit = Average Profit × 100 / Normal rate of profit

= ₹ 40,000 × 100 /10

= ₹ 4,00,000

Goodwill = Capitalised value – Capital employed

= ₹ 4,00,000 – ₹ 3,10,000

= ₹ 90,000

Question 15.

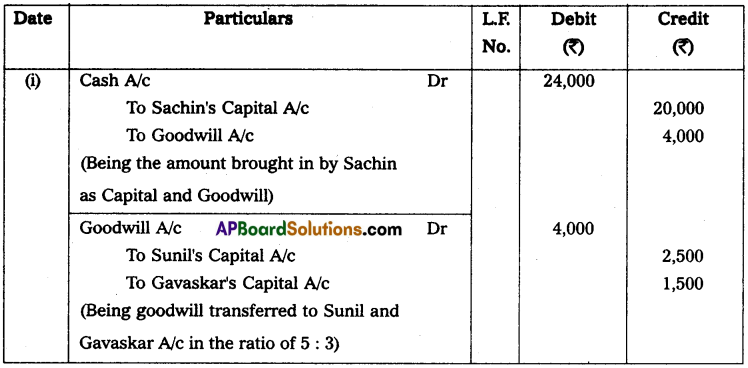

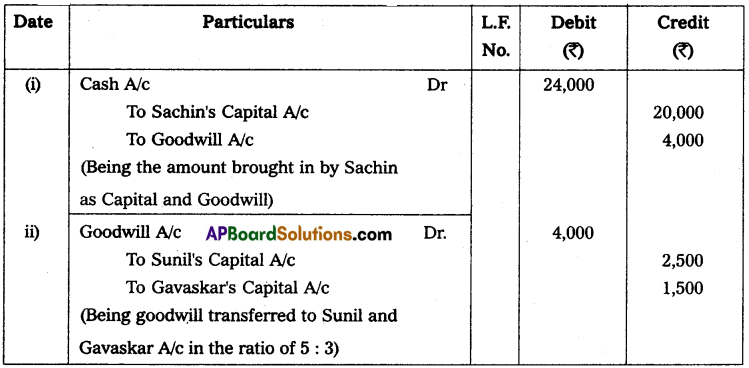

Sunil and Gavaskar are partners in the firm sharing profits and losses in the ratio of 5 : 3. Sachin is admitted to the firm for 1/5 share of profits. He is to bring in ₹ 20,000 as capital and ₹ 4,000 as bis share of goodwill. Give the necessary journal entries,

(a) When the amount of goodwill is retained in the business.

(b) When the amount of goodwill is hilly withdrawn.

(c) When 50% of the amount of goodwill is withdrawn.

Solution:

(a) When the amount of goodwill is retained in the business.

(b) When the amount of goodwill is fully withdrawn.

(c) When 50% of the amount of goodwill is withdrawn.

Question 16.

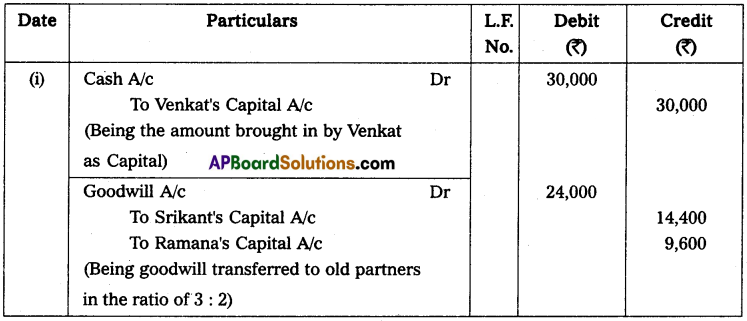

Srikant and Ramana are partners in the firm sharing profits and losses in the ratio of 3 : 2. They decide to admit Venkat into a partnership firm with 1/3 share in the profits. Venkat brings in ₹ 30,000 as his capital. On the date of admission, the goodwill has been valued at ₹ 24,000. Record the necessary journal entries in the books of the firm.

Solution:

![]()

Question 17.

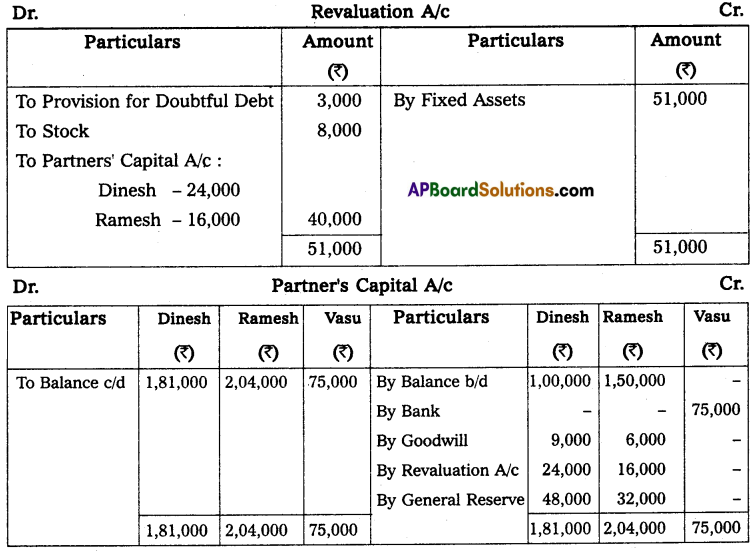

Dinesh and Ramesh are partners in the firm sharing profits and losses in the ratio of 3 : 2. They decided to admit Vasu as a partner with 1/5 share in the profits. Their Balance Sheet as on March 31, 2015, was as follows:

It was also decided that:

1. The fixed assets should be valued at ₹ 3,31,000.

2. A provision of 5% on sundry debtors to be made for doubtful debts.

3. The value of stock be reduced to ₹ 1,12,000.

4. Vasu brings ₹ 75,000 as capital and ₹ 15,000 as Goodwill.

Prepare the revised Balance sheet of the firm after admission of the partner.

Solution:

Question 18.

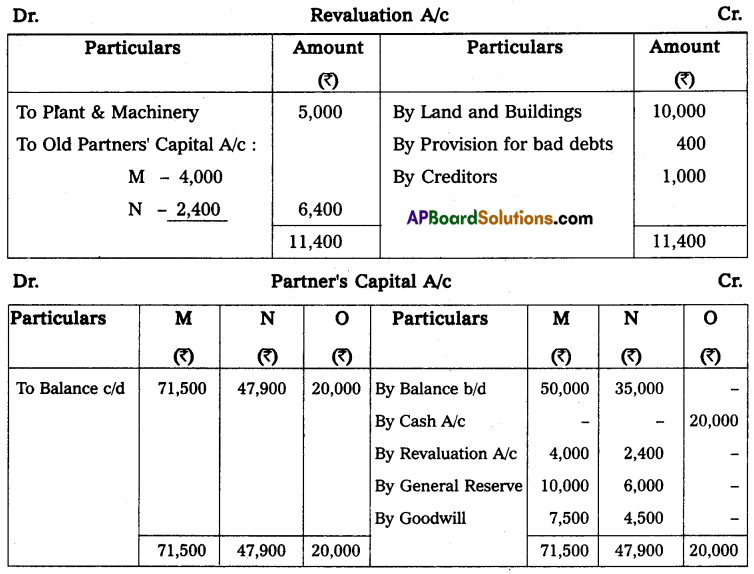

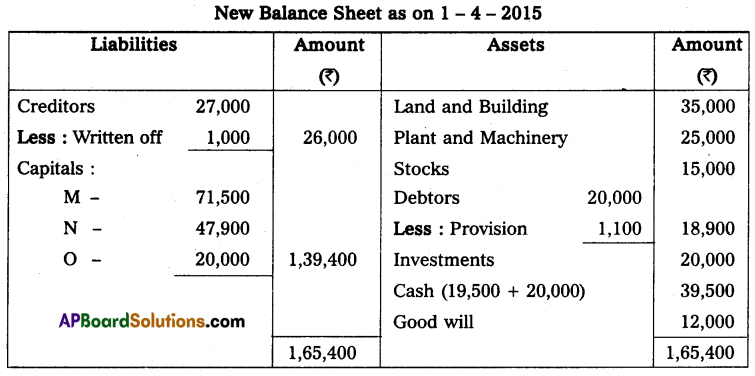

M and N were partners in the firm sharing profits in 5 : 3 ratios. They admitted O as a new partner for 1/3rd share in the profits. O was to contribute ₹ 20,000 as his capital. The Balance Sheet of M and N as of 1.4.2015 was as follows:

Other terms agreed upon were:

(i) Goodwill of the firm was valued at ₹ 12,000.

(ii) Land and buildings were to be valued at ₹ 35,000 and Plant and Machinery at ₹ 25,000.

(iii) The provision for doubtful debts was found to be in excess of ₹ 400.

(iv) A liability for ₹ 1,000 included in sundry creditors was not likely to arise.

Prepare the Revaluation Account, Partners’ Capital Accounts, and the Balance sheet of the new firm.

Solution:

Question 19.

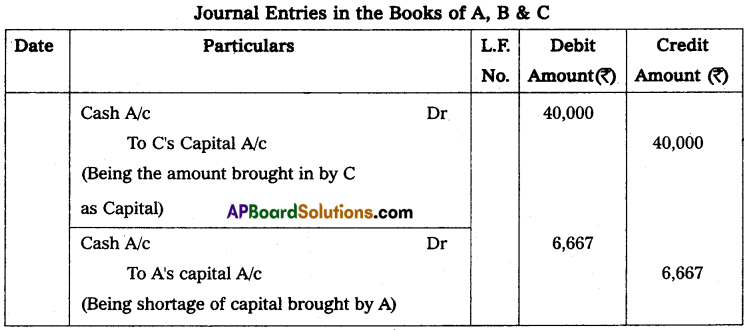

A and B are partners in a firm who are sharing profits in the ratio of 2 : 1. C is admitted into the firm for 1/5 share in profits and he is to bring in cash of ₹ 40,000 amount as his capital. The capitals of other partners are to be adjusted according to the new partner. The capital of A and B after all adjustments are ₹ 1,00,000 and ₹ 70,000 respectively. Calculate the new capitals of A and B, and record the necessary journal entries.

Solution:

Calculation of new profit sharing ratio:

If we assume the total share is 1

The new partner C’s share = \(\frac{1}{5}\) share out of 1

Rest of the share = 1 – \(\frac{1}{5}\) = \(\frac{4}{5}\)

A’s new share = \(\frac{4}{5} \times \frac{2}{3}=\frac{8}{15}\)

B’s new share = \(\frac{4}{5} \times \frac{1}{3}=\frac{4}{15}\)

New partner C’s capital for 1/5th share = 40,000

The total capital of the firm = 40,000 × \(\frac{5}{1}\) = ₹ 2,00,000

A’s new capital = 2,00,000 × \(\frac{8}{15}\) = ₹ 1,06,667

B’s new capital = 2,00,000 × \(\frac{4}{15}\) = ₹ 53,333

Hence, a will bring in ₹ 6,667 (₹ 1,06,667 – ₹ 1,00,000)

B will withdraw ₹ 16,667 (₹ 70,000 – ₹ 53,333)

The journal entries in this regard will be recorded as follows:

![]()

Question 20.

A and B share profits in the proportions of 3/5 and 2/5. Their Balance Sheet on Dec. 31, 2014, was as follows:

On that date C was admitted into partnership on the following terms:

(a) That C pays ₹ 10,000 as his capital and ₹ 5,000 as goodwill for his 1/6th share in profits.

(b) That stock and fixtures be reduced by 10% and 5% provision for doubtful debts be created on Sundry Debtors and Bills Receivables.

(c) That the value of land and buildings be appreciated by 20%.

Prepare necessary Accounts and the new Balance Sheet on the admission of C.

Solution:

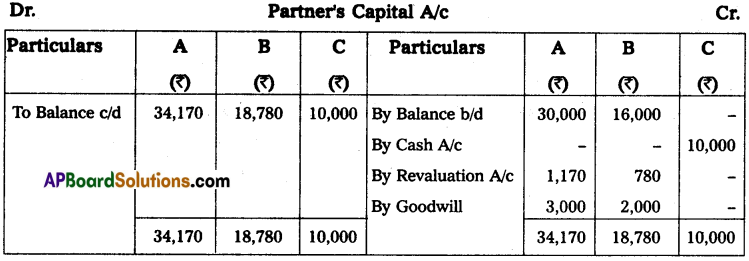

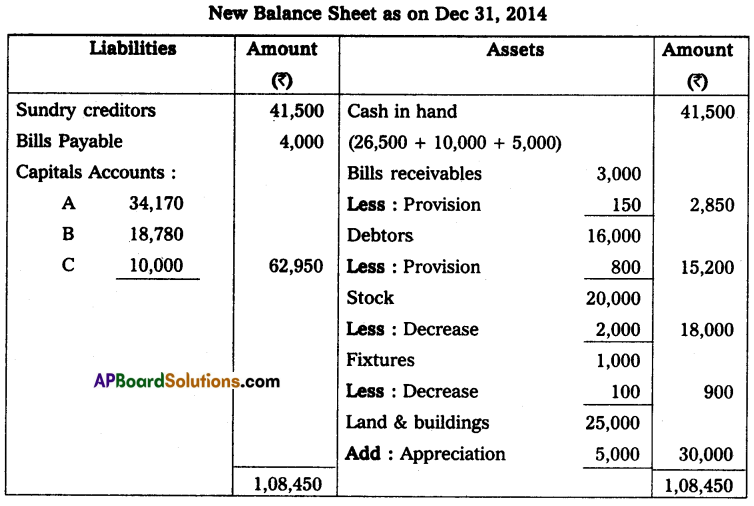

Question 21.

On 31st March 2014, the Balance sheet of P and Q shared profits in 3 : 2 ratio was as follows:

On that date, R was admitted as a partner on the following conditions:

(a) R will get a 4/15th share of profits. R had to bring ₹ 60,000 as his capital.

(b) The assets would be revalued as under:

Sundry debtors at book value less 5% provision for bad debts. Stock at ₹ 40,000, plant and Machinery at ₹ 80,000.

Prepare Revaluation A/c, Partner’s Capital A/c, and the Balance Sheet of the new firm.

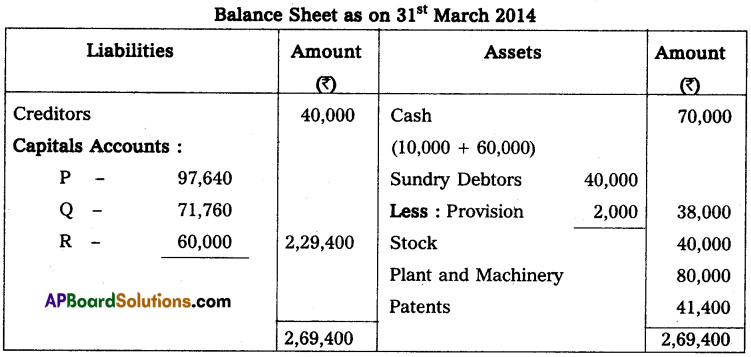

Solution:

![]()

Question 22.

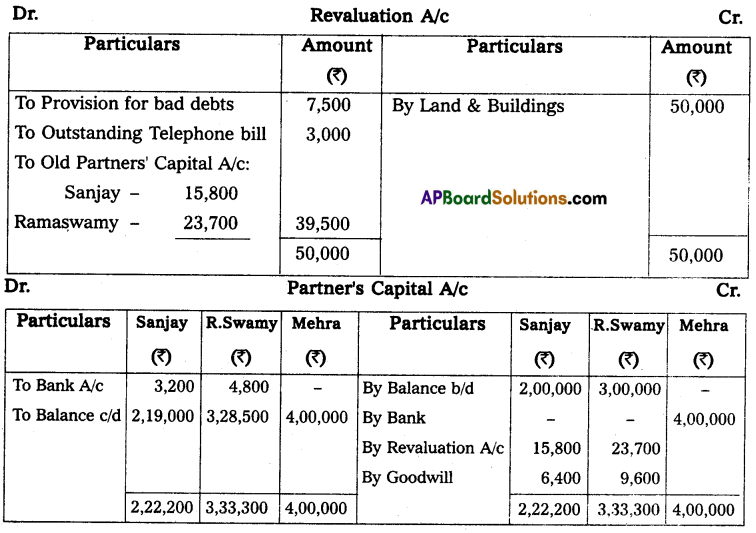

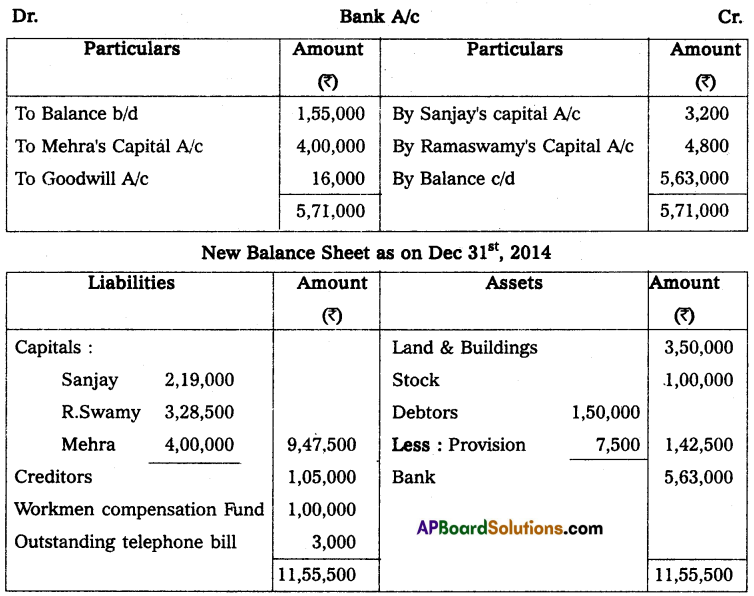

Sanjay and Ramaswamy were partners in a firm sharing the profits in the ratio of 2 : 3. On 31-03-2015 they admitted Mehra as a new partner for 1/5th share in the profits. Their balance sheet was as follows:

On Mehra’s admission, it was agreed that:

1. Mehra will bring ₹ 4,00,000 as his capital and ₹ 16,000 for his share of goodwill, half of which was withdrawn by Sanjay and Ramaswamy.

2. A provision of 5% for bad and doubtful debts was to be created.

3. A provision was to be made for outstanding telephone bills of ₹ 3,000.

4. Land and Buildings are valued at ₹ 3,50,000.

After the above adjustments prepare the necessary accounts and the new balance sheet.

Solution: