Andhra Pradesh BIEAP AP Inter 1st Year Economics Study Material 4th Lesson Theory of Production Textbook Questions and Answers.

AP Inter 1st Year Economics Study Material 4th Lesson Theory of Production

Essay Questions

Question 1.

Explain the law of variable proportions. [March 18, 17]

Answer:

The law of variable proportions has been developed by the 19th-century economists David Ricardo and Marshall. The law is associated with the names of these two economists. The law states that by increasing one variable factor and keeping other factors constant, how to change the level of output, total output first increases at an increasing rate, then at a diminishing rate and later decreases. Hence this law is also known as the “Law of Diminishing returns”.

Marshall stated in the following words.

“An increase in capital and labour applied in the cultivation of land causes, in general, less than proportionate increase in the amount of produce raised, unless it happens to coincide with an improvement in the arts of agriculture”.

Assumptions :

- The state of technology remain constant.

- The analysis relates to short period.

- The law assumes labour in homogeneous.

- Input prices remain unchanged.

Explanation of the Law :

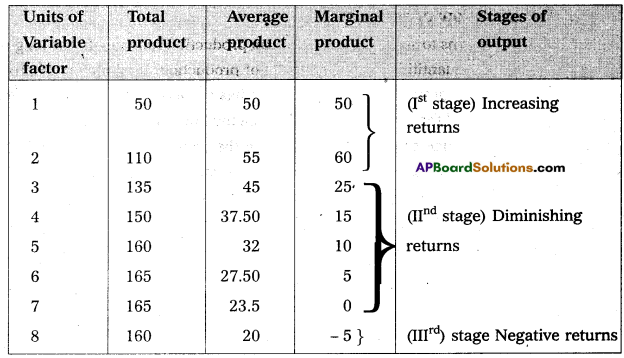

Suppose a farmer has ‘4’ acres of land he wants to increase output by increasing the number of labourers, keeping other factors constant. The changes in total production, average product and marginal product can be observed in the following table.

In the above table total product refers to the total output produced per unit of time by all the labourers employed.

Average product refers to the product per unit of labour marginal product refers to additional product obtained by employing an additional labour.

In the above table there are three stages of production.

1st stage i.e., increasing returns at 2 units total output increases average product increases and marginal product reaches maximum.

2nd stage i.e., diminishing returns from 3rd unit onwards TP increases diminishing rate and reaches maximum, MP becomes zero, AP continuously decreases.

3rd stage i.e., negative returns from 8th unit TP decreases AP declines and MP becomes negative.

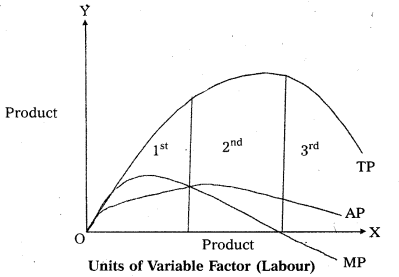

This can be explained in the following diagram.

In the diagram on ‘OX’, axis shown units labourer and OY’ axis show TP, MP, and AP. 1st stage TP, AP increases MP is maximum. In the 2nd stage TP maximum, AP MP is zero. At 3rd stage TP declines, AP also declines, MP becomes negative.

![]()

Question 2.

Explain the law of returns to scale.

Answer:

The law of returns to scale relate to long run production function. In the long run it is possible to alter the quantities of all the factors of production. If all factors of production are increased in given proportion the total output has to increase in the same proportion. Ex : The amounts of all the factors are doubled, the total output has to be doubled increasing all factors in the same proportion is increasing the scale of operation. When all inputs are changed in a given proportion, then the output is changed in the same proportion. We have constant returns to scale and finally arises diminishing returns. Hence as a result of change in the scale of production, total product increases at increasing rate, then at a constant rate and finally at a diminishing rate.

Assumptions :

- All inputs are variable.

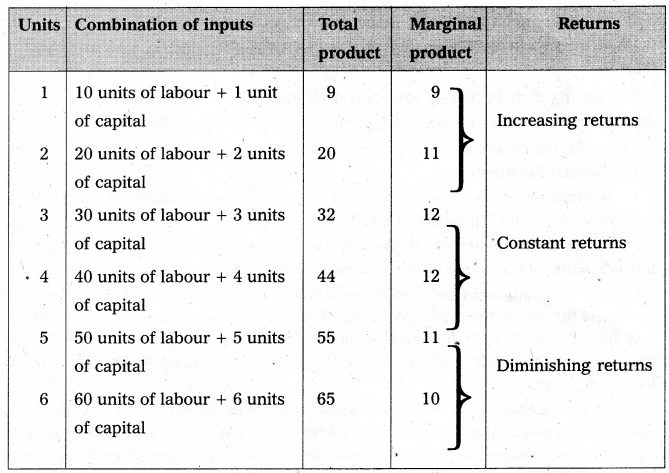

- It assumes that state of technology remain the same. The returns to scale can be shown in the following table.

The above table reveals the three patterns of returns to scale. In the 1th place, when the scale is expanded upto 3 units, the returns are increasing. Later and upto 4th units, it remains constant and finally from 5th on words the returns go on diminishing.

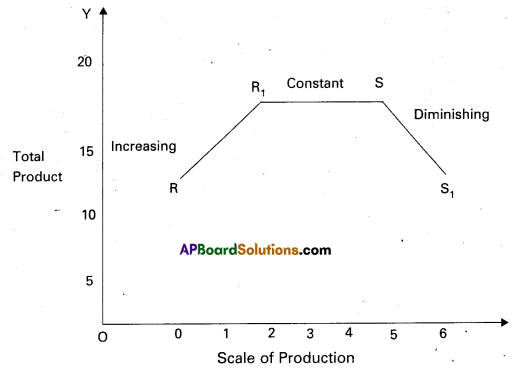

In the diagram on ‘OX’ axis shown scale of production, on OY’ axis shown total product. RR1 represents increasing returns R1S – Constant returns; SS1 represents diminishing returns.

![]()

Question 3.

Distinguish between internal and external economies.

Answer:

Economies of large scale production can be grouped into two types.

- Internal economies

- External economies.

1. Internal Economies:

Internal economies are those which arise from the expansion of the plant, size or from its own growth. These are enjoyed by that firm only.

“Internal economies are those which are open to a single factory or a single firm independently of the action of other firms”. – Cairncross

i) Technological Economies : The firm may be running many productive establishments. As the size of the productive establishments increase, some mechanical advantages may be obtained. Economies can be obtained from linking process to another process i.e. paper making and pulp making can be combined. It also used superior techniques and increased specialization.

ii) Managerial Economies : Managerial economies arises from specialisation of management and mechanisation of managerial functions. For a large size firm it becomes possible for the management to divide itself into specialised departments under specialised personnel. This increases efficiency of management at all levels. Large firms have the opportunity to use advanced techniques of communication, computers etc. All these things help in saving of time and improve the efficiency of the management.

iii) Marketing Economies : The large firm can buy raw materials cheaply, because it buys in bulk. It can secure special concession rates from transport agencies. The product can be advertise better. It will be able to sell better.

iv) Financial Economies : A large firm can arise funds more easily and cheaply a small one. It can borrow from bankers upon better security.

v) Risk bearing Economies : A large firm incurs unrisk and it can also reduce risks. It can spread risks in different ways. It can undertake diversifications of output. It can buy raw materials from several firms.

vi) Labour Economies : A big firm employs a large number of workers. Each worker is given the kind of job he is fit for.

2. External Economies :

An external economy is one which is available to all the firms in an industry. External economies are available as an industry grows in size.

- Economies of Concentration : When a number pf firms producing an identical product are localised in one place, certain facilities become available to all. Ex : Cheap transport facility, availability of skilled labour etc.

- Economies of Information : When the number of firms in an industry increases collective action and co-operative effort becomes possible. Research work can be carried on jointly. Scientific journal can be published. There is possibility for exchange of ideas.

- Economies of Disintegration : When the number of firms increases, the firm may agree to specialise. They may divide among themselves the type of products of stages of production. Ex : Cotton industry.

![]()

Question 4.

Explain short-run cost structure of a Firm.

Answer:

Costs are divided into two categories i.e.,

- Short run cost curves

- Long run cost curves.

In short run by increasing only one factor i.e., (labour) and keeping other factor constant. The short run cost are again divided into two types.

- General costs

- Economic costs.

1. General costs :

i) Money costs : Production is the outcome of the efforts of factors of production like land, labour, capital and organisation. So, rent to land, wage to labour, interest to capital and profits to entrepreneur has to paid in the form of money is called money cost.

ii) Real cost: Adam Smith regarded pains and sacrifices of labour as real cost. So it cannot be measured interms of money.

iii) Opportunity cost: Factors of production are scarce and have alternative uses. The opportunity cost of a factor is the benefit that is foregone from the next best alternative use.

2. Economic costs :

i) Fixed costs : The cost of production which remains constant even the production may be increase or decrease is known as fixed cost. The amount spent by the cost of plant and equipment, permanent staff are treated as fixed costs.

ii) Variable cost: The cost of production which is changing according to changes in the production is said to be variable cost. In the long period all costs are variable costs. It include price of raw materials, payment of fuel, excise taxes etc. Marshall called “Prime cost”.

iii) Average cost: Average cost means cost per units of output. If we divided total cost by the number of units produced, we will get average cost.

AC = \(\frac{\text { Total cost }}{\text { Output }}\)

iv) Marginal cost: Marginal cost is the additional cost of production producing one more unit.

MC = \(\frac{\Delta \mathrm{TC}}{\Delta \mathrm{Q}}\)

v) Total cost: Total cost is the sum of total fixed cost and total variable cost.

TC = FC + VC

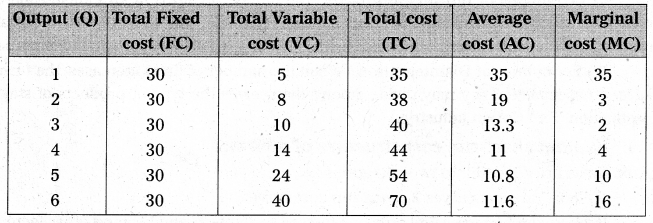

The short term cost in relation to output are explained with the help of a table.

In the above table shows that as output is increased in the 1st column, fixed cost remains constant. Variable costs have changed as and when there are changes in output. To produce more output in the short period, more variable factors have to be employed. By adding FC & VC we get total cost different levels of output. AC falls output increases, reaches its minimum and then rises MC also change in the total cost associated with a change in output. This can be shown in the diagram.

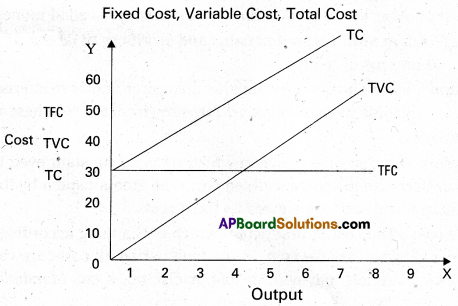

In the above diagram on ‘OX’ axis taken by output and ‘OY taken by costs. The shapes of different cost curves explain the relationship between output and different costs. TFC is horizontal to ‘X’ axis. It indicates that increase in output has no effect on fixed cost. TVC on the other side increases along with level of output. TC curve rises as output increases.

Additional Questions

Question 1.

Explain Production function.

Answer:

Production function is technical concept. It explains the physical relationship between input and output at any period of time. It represents functional relationship between inputs and the amount of output produced.

According to Stigler “Production is the name given to the relationship between rates of inputs of productive services and the rate of output of product”.

The production function can be expressed mathematically as follows.

Gx = f (L, K, R, N, T)

Gx = Output

f = Functional relationship

L = Amount of Labour

K = Amount of Capital

R = Raw material

N = Natural resources or land

T = State of Technology.

Where Gx is dependent variable and is determined by the inputs used, whereas L, K, R, N, T are independent variables.

![]()

Question 2.

Explain Law of supply.

Answer:

The law of supply explains the functional relationship between price of a commodity and its quantity supplied. The law of supply can be stated as follows “Other things remaining the same, as the price of a commodity rises its supply is extended and as the price falls its supply is contracted”.

The law of supply can be explained with the help of supply schedule and supply curve.

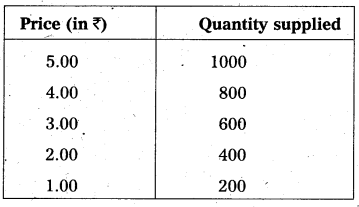

Supply Schedule : Supply schedule explains various amounts of good that the seller offers for sale at different prices. It represents the functional relationship between price and quantities supplied. There is direct relationship between price and supply. This can be shown in the following schedule.

The above schedule high price i.e, ₹ 5.00 per unit 1000 units are supplied and at ₹ 1 per 200 units are supplied. It means high price indicate high supply and low price indicates low supply. So, it shows the direct relationship between price and supply.

Supply curve :

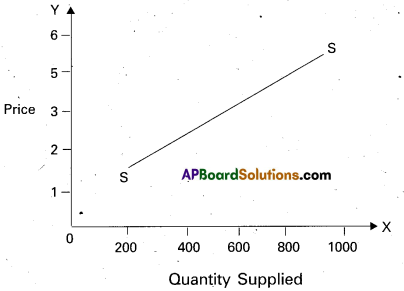

A supply curve can be drawn with the help of above supply schedule to explain the direct relationship between price and supply.

In the above diagram supply is shown on ‘OX’ axis and price is shown ‘OY axis. SS is supply curve. It slopes upwards from left to right. The slope of supply curve is always positive. Because there is direct relationship between the price and supply.’

Question 3.

Define Factors of production.

Answer:

Factors that help in the production process are called factors of production.

Ex : land, labour, capital and organization

1) Land : Land stands in economics for natural resources. There are nature given resources like soil, earth, water, rainfall, forests, mines, clijnate etc. All these come under land. Land is the productive equipment given by nature. The remuneration to land is called rent.

2) Labour : Labour is man’s effort. It may be physical or mental labour. Any service offered for a price is considered as labour in economics. All services rendered to produce scarce goods come under labour. The remuneration to labour is called wage.

3) Capital : Capital is man made production equipment. Factories, buildings, vehicles, rail-roads, roads, irrigation dam etc., come under capital. The remuneration to capital is interest.

4) Organisation or Entrepreneurship : The entrepreneur or businessmen brings together all the factors of production required for production. He bears the risk is doing so. He coordinates the functions of different factors. Profit is the remuneration for organisation or entrepreneurship.

![]()

Question 4.

Define land and explain the characteristics of land.

Answer:

Land stands in economics for natural resources. There are nature given resources like soil, earth, water, rainfall, forests, mines, climate etc., all these come under land. Land is the productive, equipment given by nature. The remuneration to land is called rent. Characteristics of land:

- Land is a free gift of nature.

- The supply of land is perfectly inelastic from the point of view of economy.

- Land cannot be shifted from one place to another place.

- It does not yield any result unless human effort’s are employed.

Question 5.

Define labour. Explain the characteristics of labour.

Answer:

Labour is man’s effort. It may be physical (or) mental labour. Any’service offered for a price is considered as labour in economics. The remuneration to labour is called wage. Characteristics of labour:

- Labour is inseparable from the labourer himself.

- Labour is highly ‘perishable’. It means labour lost cannot store his labour.

- Labour has a very weak bargaining power.

- Labour power differs from labourer to labourer of their skills.

- The supply curve of a labourer is backward bending.

Question 6.

What is supply ? What are the determinants of supply.

Answer:

The supply of a commodity means the total quantity of the commodity that sellers offer to sell at different prices from the stock of that commodity existing at any given time. The supply of commodity depends upon the following factors.

Determinants of supply :

- Price of the commodity: The supply of the commodity depends upon the price of that commodity. When price falls, supply falls and when price rises, supply also rises. Thus price and supply are directly related.

- Factor prices : The cost of production of a commodity depends upon the prices of various factors of production.

- Prices of related goods : The supply of the commodity depends upon the prices of related goods. If the price of a substitute good goes up, the producer will be induced to

- State of technology: Technological improvements determine supply of a commodity. Progress in technology leads to reduction in the cost of production which will increase supply.

- Government policy : Imposition of heavy taxes as a commodity discourages its production. Hence production decreases.

![]()

Question 7.

Explain the nature of revenue curves untier perfect competition.

Answer:

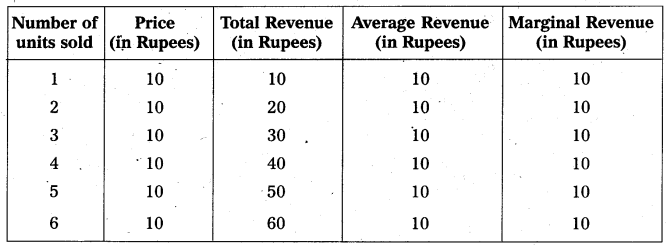

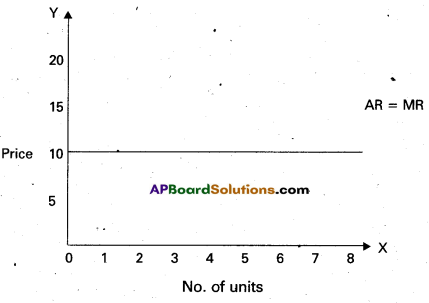

If competition is perfect in market, the market is known as perfectly competitive market. Due to the existing features the total demand and total supply pf a commodity interact to determine the price in the industry and individual firm. Hence, an individual seller or firm is a price taker but not a price maker in perfect competition, ‘therefore he can sell any quantity at the ruling price. Thus, the demand curve is parallel to X-axis. The nature of Average Revenue (AR) and Marginal Revenue (MR) and their relationship under perfect competition can be better understood from the following schedule.

Revenue Schedule :

The above table indicates that in perfect competition price remains the same irrespective of the number of units sold. Therefore, the total revenue increases at a constant rate. AR and MR are equal. There is no difference among price AR and MR. This can be reveals the following diagram.

In the diagram X-axis represents number of units (output) and Y-axis represents revenue. DP is demand curve.

In diagram, the Average Revenue curve (AR) is horizontal straight line parallel to the X-axis and Marginal Revenue Curve MR coincides with it. Because the seller can sell number of units given the price, the AR curve facing the seller is a horizontal line.

Very Short Answer Questions

Question 1.

Production function [March 18]

Answer:

The production function is the none for the relation between the physical inputs and the physical outputs of a film. Production of a firm, production function explains the functional relationship between inputs and outputs this can be as follows Gx = f (L, K, R, N, T).

![]()

Question 2.

Law of supply [March 16]

Answer:

The law of supply explains the functional relationship between price of a commodity and its quantity supplied. The law of supply can be stated as follows. “Other things remaining the same, as the price of a commodity rises its supply is extended and as the price falls its supply is contracted”.

Question 3.

Factors of production

Answer:

Factors that help in the production process are called factors of production.

Ex : land, labour, capital and organization.

Question 4.

Average cost

Answer:

If we divided total cost, by the number of units produced. We will get average cost. Average cost means cost per unit of output.

AC = \(\frac{\mathrm{TC}}{\text { Output }}\)

Question 5.

Marginal cost

Answer:

Marginal cost is the additional cost of production producing one more unit in other words it is the addition made to total cost by producing one more unit of a commodity.

MC = \(\frac{\Delta \mathrm{TC}}{\Delta \mathrm{Q}}\)

Additional Questions

Question 6.

Production

Answer:

Production is the process that converts inputs into output in economies production includes services along with physical goods.

![]()

Question 7.

Short period

Answer:

Short period is a period in which a producer is unable to change factors of production to increase output. This relates to law of variable proportions.

Question 8.

Long period

Answer:

Long period is a period in which a producer is unable to change factors of production to increase output. This relates to returns to scale.

Question 9.

Average product

Answer:

It refers to the product per unit of labour it is Obtained by dividing total product by the number of labourers employed.

AP = \(\frac{\mathrm{TP}}{\mathrm{L}}\)

Question 10.

Marginal product

Answer:

It is the additional product by employing an additional labour.

MP = \(\frac{\Delta \mathrm{TP}}{\Delta \mathrm{L}}\)

Question 11.

Fixed factor

Answer:

Fixed factors are those costs which can’t be changed by the producer in the short period.

Ex : Buildings, Machinery etc.

Question 12.

Variable factors

Answer:

The factors of production which are possible to change in relation to a change in output is known as variable factors in the long run all factors of production are variable.

Ex : Labour, Raw materials.

![]()

Question 13.

Change in scale of production

Answer:

It refers that output will be increase by increasing inputs in the long period.

Question 14.

Internal economies

Answer:

It refers that when a firm expands output by increasing all inputs.

Question 15.

External economics

Answer:

It refers to one which is available to all the firms in an industry. External economies are available as an industry grows in size.

Question 16.

Supply

Answer:

The quantity of a commodity that a seller is prepared to sell at a particular price and at a particular time is known as supply. The supply curve slopes upwards from left to right.

Question 17.

Supply function

Answer:

It explains the functional relation between supply and the factors of production of a good.

Question 18.

Opportunity cost

Answer:

The opportunity cost of a factor is the benefit i.e, forgone from the next best alternative use.

![]()

Question 19.

Fixed cost

Answer:

The cost of production which remains constant even the production may be increase (or) decrease is known as fixed cost.

Ex : Machinery, permanent staff salaries.

Question 20.

Variable cost

Answer:

The cost of production which is changed according to changes in the production is said to be variable cost. In the long period all costs are variable costs it include price of raw materials, wages of labour, power transport charges etc.

Question 21.

Total Revenue

Answer:

Total revenue of a producer depends on the price and the quantity of output sold in the market.

Total Revenue = Price × Quantity of output

TR = P × Q

Question 22.

Average Revenue

Answer:

Average revenue is the revenue per unit of output. Average revenue is obtained by dividing to revenue by the number of unit sold.

AR = \(\frac{\text { TR }}{\mathrm{Q}}\)

Question 23.

Marginal Revenue

Answer:

Marginal revenue is the additional revenue earned by selling one more unit of the product. In other words change in total revenue arising from the sale of an additional unit of output is called marginal revenue.

MR = \(\frac{\Delta \mathrm{TR}}{\Delta \mathrm{Q}}\)

![]()

Question 24.

Total Cost

Answer:

Total cost can be obtained by adding total fixed costs and variable costs.